How a fintech provider replaced a complex payments flow with a single score

Every ACH retry triggered a balance check that couldn't tell a pull that would settle from one that would bounce. So the provider stopped buying the check and scored the retry instead.

Challenge

Run collections at this volume and every fraction of a cent compounds. The provider paid for a balance check on every single retry, more than 760,000 times a month, adding up to tens of thousands of dollars a month it could read straight off the invoice.

Here is the part that should bother any risk team: the check didn't work. "There is money in the account right now" is not the same as "this debit will clear." Retries that passed the check cleanly came back as returns. Retries that would have settled never got attempted. The provider was paying a premium for a signal that couldn't sort a good retry from a bad one.

A lower-cost check wouldn't fix that. The provider needed a signal sharp enough to make the check pointless.

Solution

So the provider stopped shopping for a better check and started scoring the retry. Pave's ACH Risk Score reads each attempt before it goes out, and it runs on the Pave Cashflow Data the provider was already using to underwrite. No new integration, just one more call on data it already trusted.

The score gets its edge from feedback: every attempt and its outcome flow back into the model, across every lender on the network, so it learns which retries actually settle. Pave's data science team set the cutoff with the provider's risk team, to their goals, then ran it in the open. A two-week shadow test confirmed the score behaved in production the way it did in the backtest. The team could see the numbers before betting a dollar on them. Then they turned it on.

Approach

Results

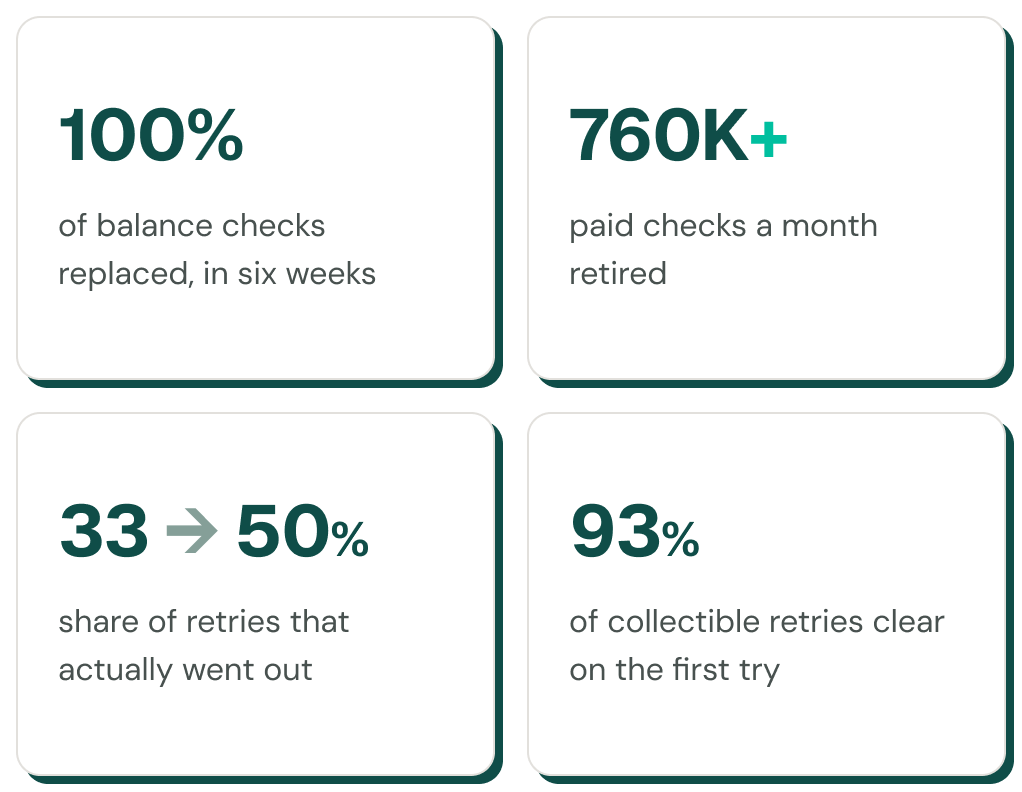

100% of balance checks replaced in six weeks. A 760,000-call-a-month paid check, retired, and tens of thousands of dollars a month in per-call cost with it.

Attempts that actually went out rose from 33% to 50%, with 93% of collectible retries landing on the first try.

The score didn't just cost less than the check. It did the job the check couldn't: tell a retry that would clear from one that would bounce before the pull. And because every one of those outcomes feeds back into the model, it keeps getting sharper.

"The moment that was true, paying per call was a habit, not a strategy."

Conclusion

Replacing a balance check with a score isn't swapping one tool for another. It's a provider realizing it was paying a vendor to answer a question its own data already answered. Anyone running ACH collections at scale is in the same spot: the per-call bill grows with volume, and a point-in-time balance check says almost nothing about whether a debit will clear. Once the cashflow data is already in the building, the retry decision costs one more score, not one more paid check. The provider now runs the score on every retry.

See what a score built for your book can do

Off-the-shelf scores you can deploy today, sharpened by every lender on the network.

Explore Use Cases

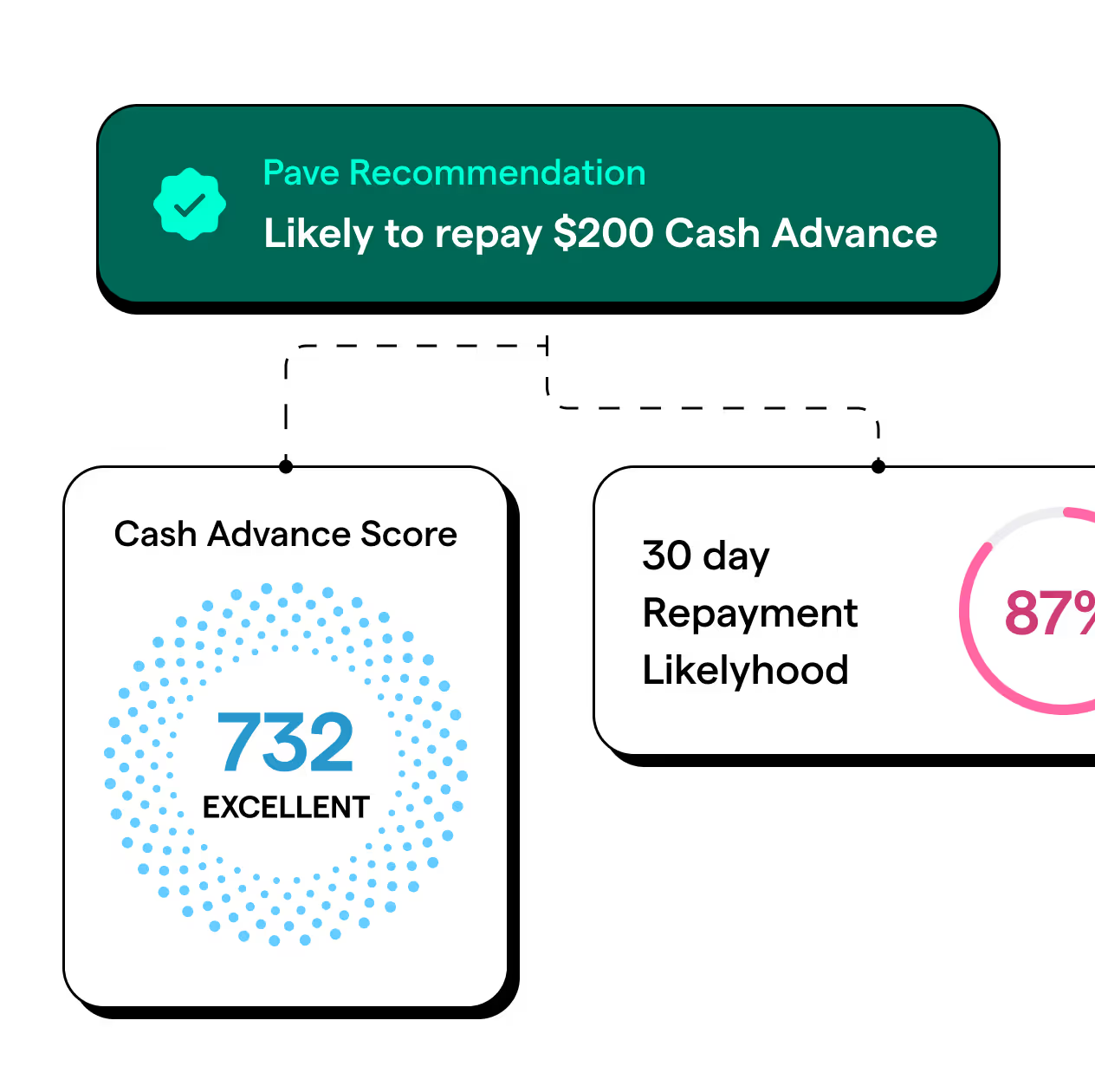

Cash Advance

Score users to increase approvals, advance amounts, and improve repayments.

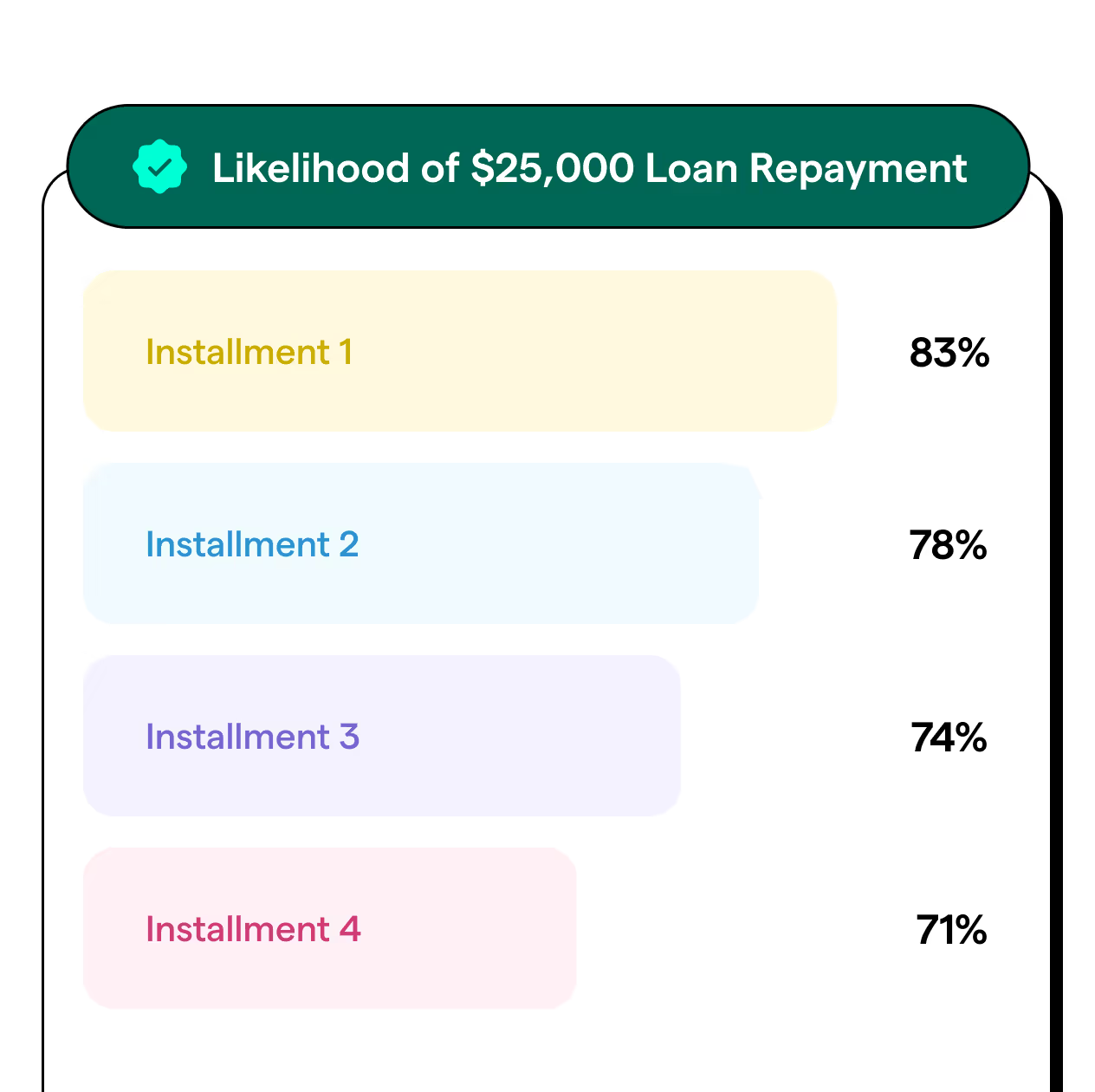

Personal Loans

Identify users with high likelihood of making the first 4 payments to reduce delinquencies.

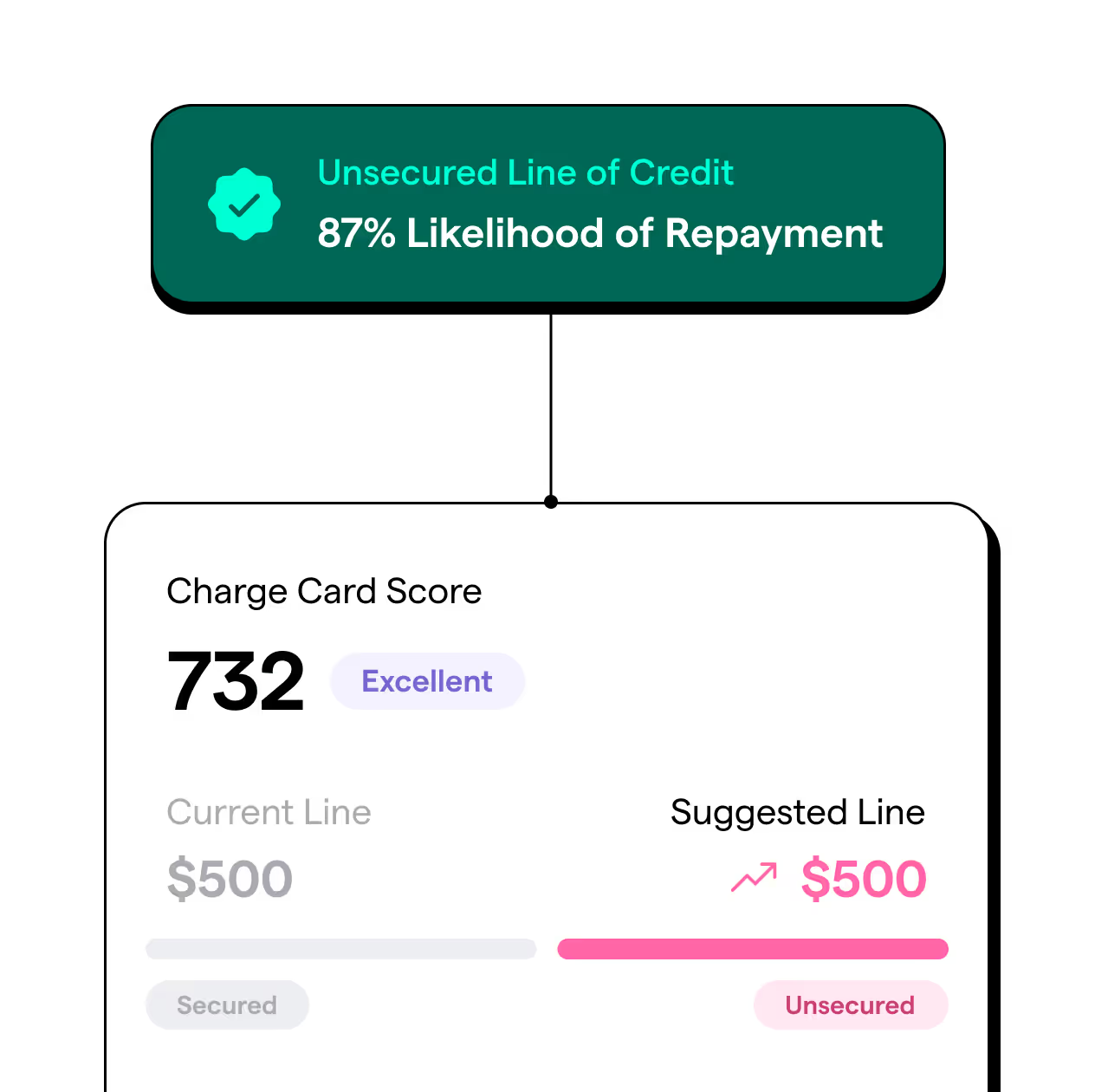

Charge Cards

Graduate users to higher secured or unsecured limits based on increased affordability.

Credit Cards

Set dynamic credit limits based on users' income and affordability.

Drive growth with Cashflow-driven Analytics

Use our Cashflow-driven Attributes and Scores to provide timely, borrower-specific insights tailored to your lending criteria. Make informed decisions that enhance approval rates and loan performance.