Credit Card Underwriting & Risk Analytics

Dynamically adjust credit limits with Cashflow-driven Attributes and Scores that leverage real-time data for more informed risk decisions.

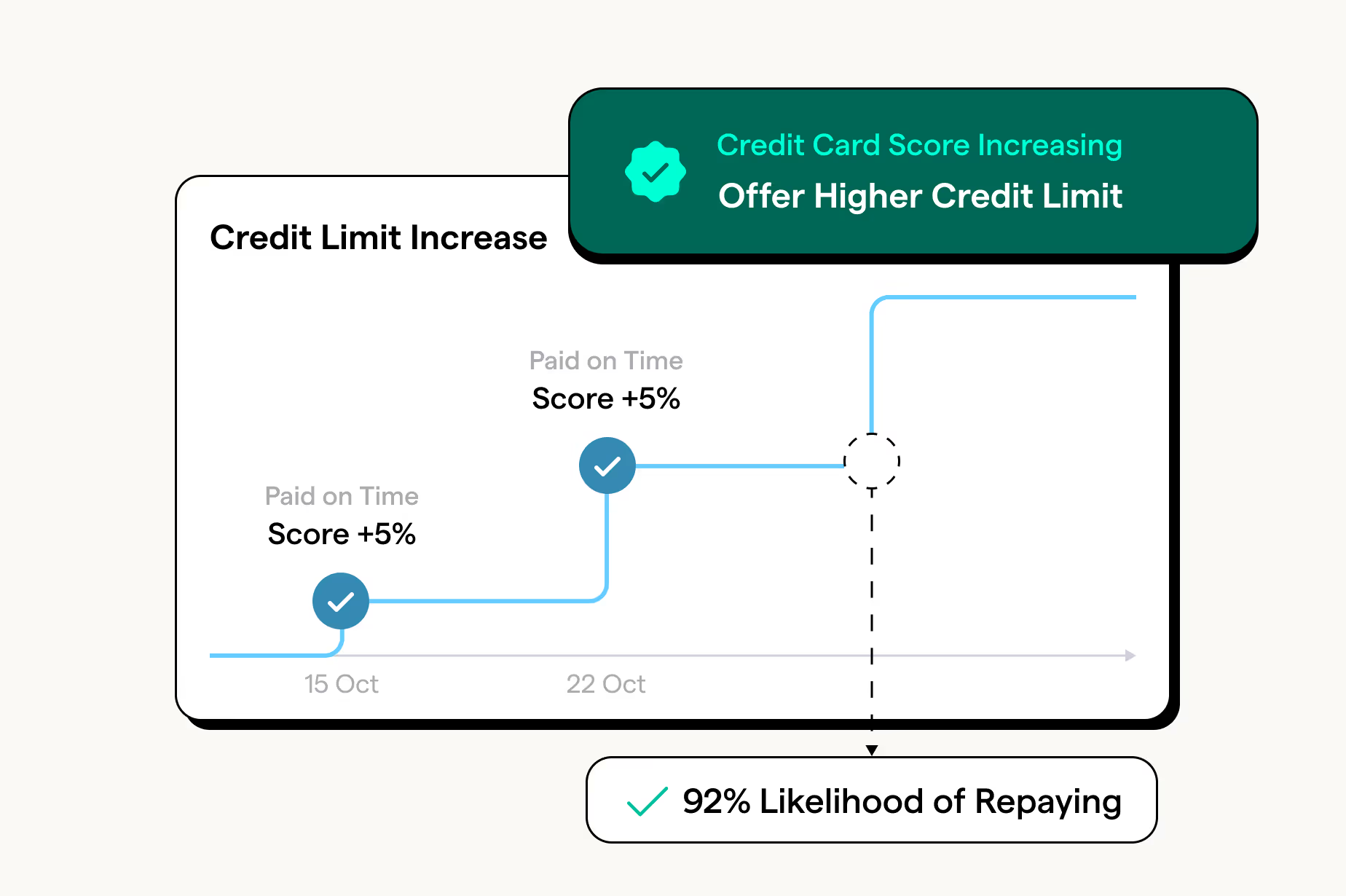

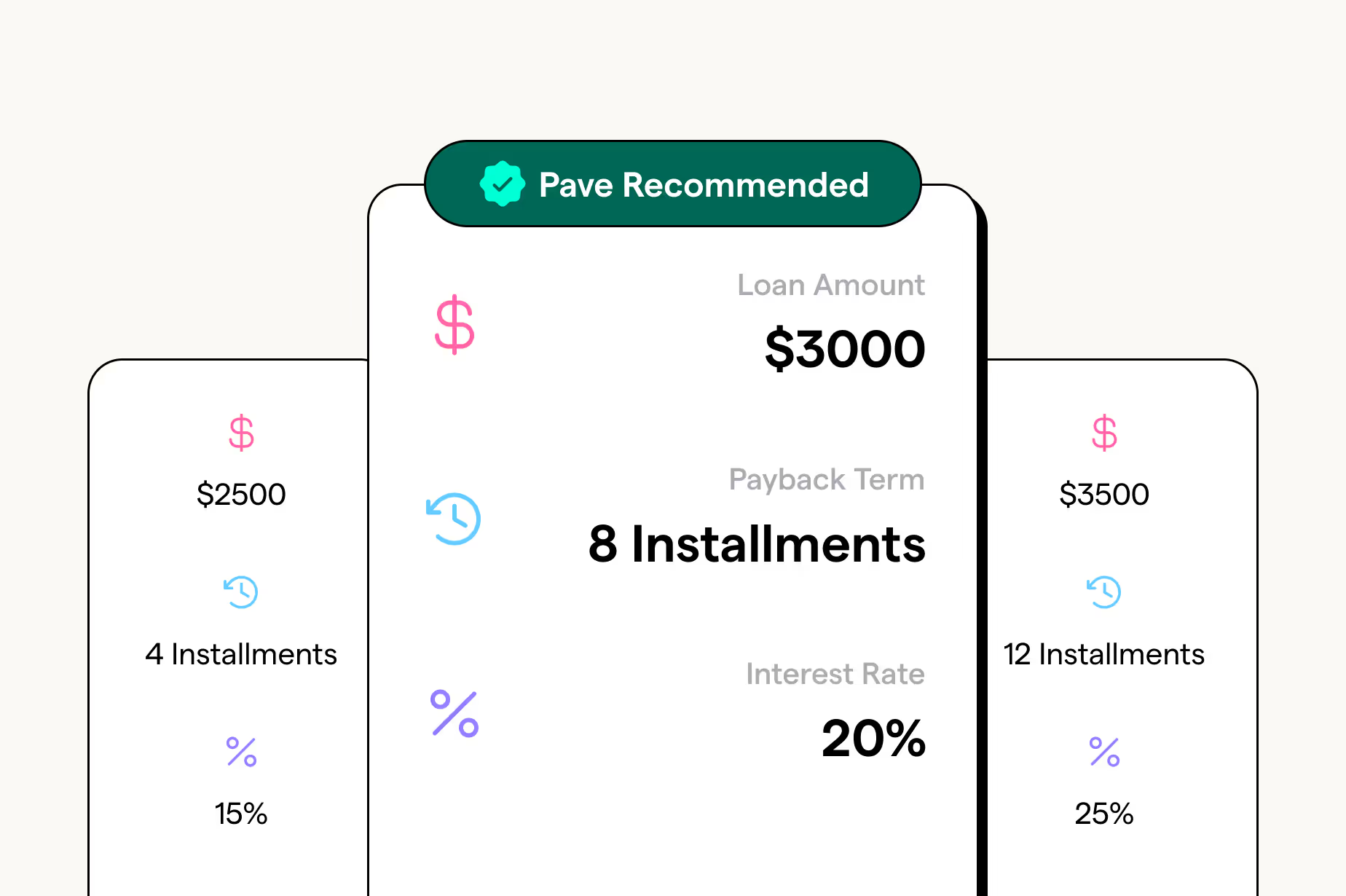

Drive Growth with Predictive Cashflow-Driven Credit Limit Increases

Leverage real-time Cashflow Analytics to enhance account monitoring across credit tiers and set credit limits aligned with user affordability.

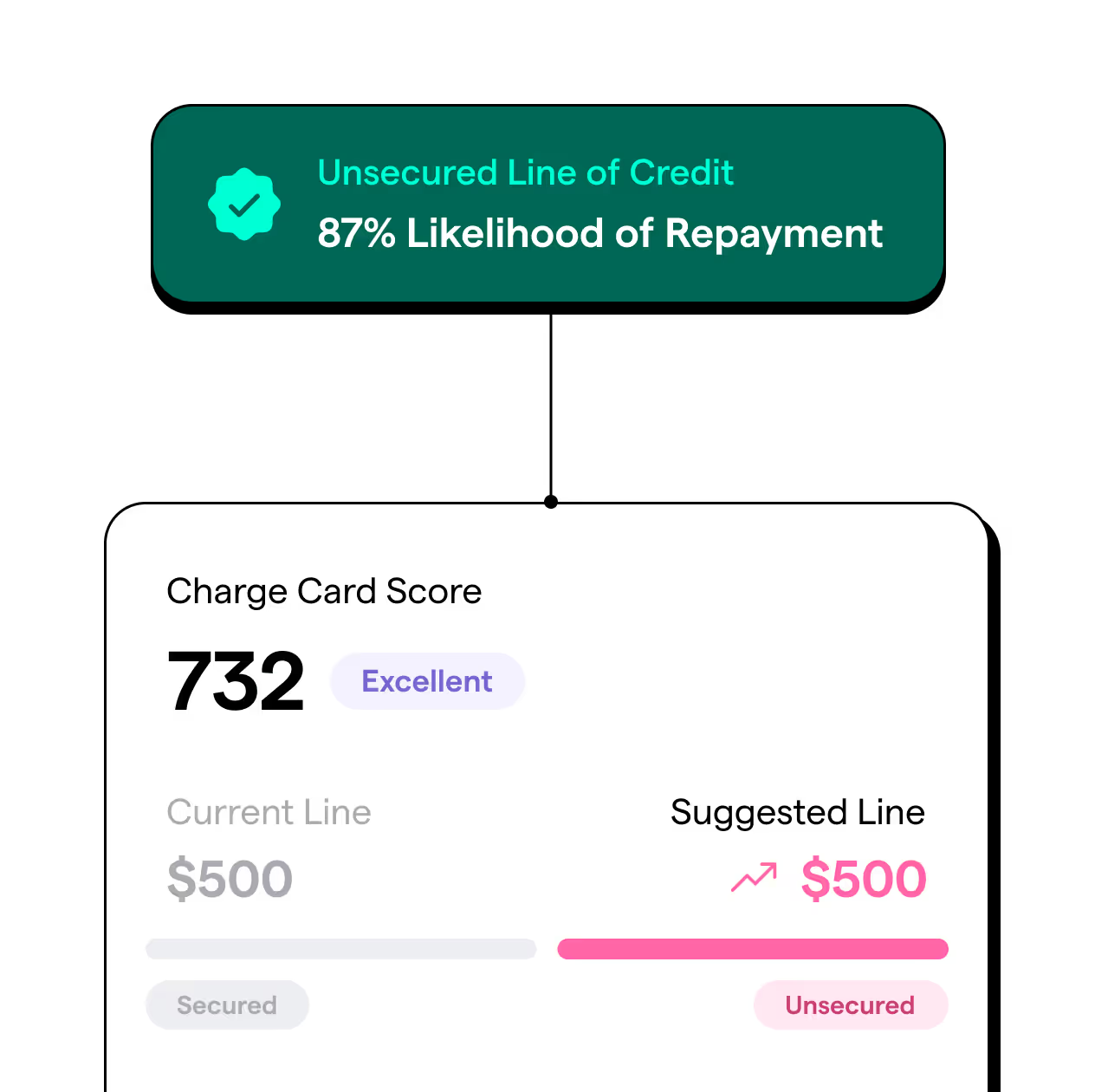

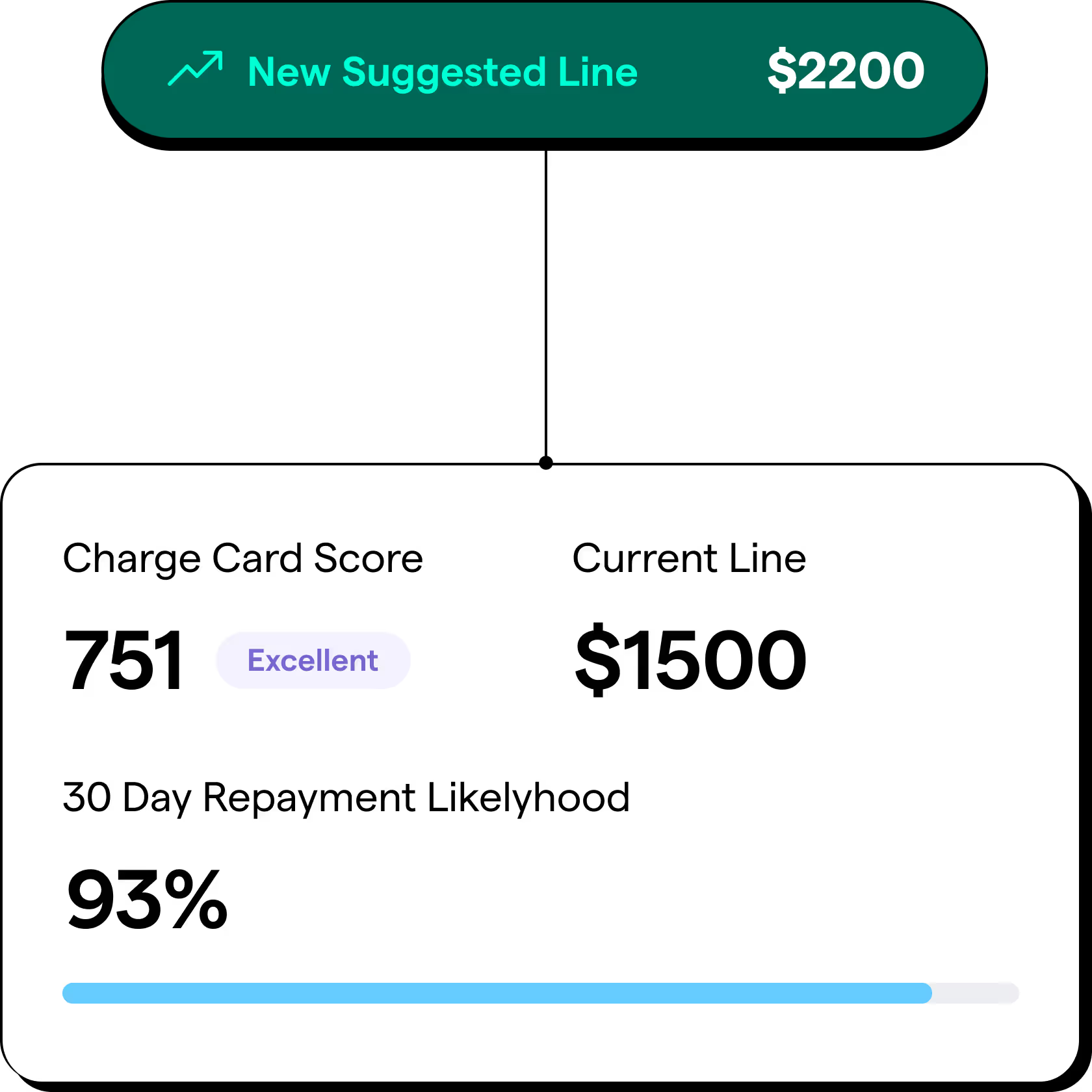

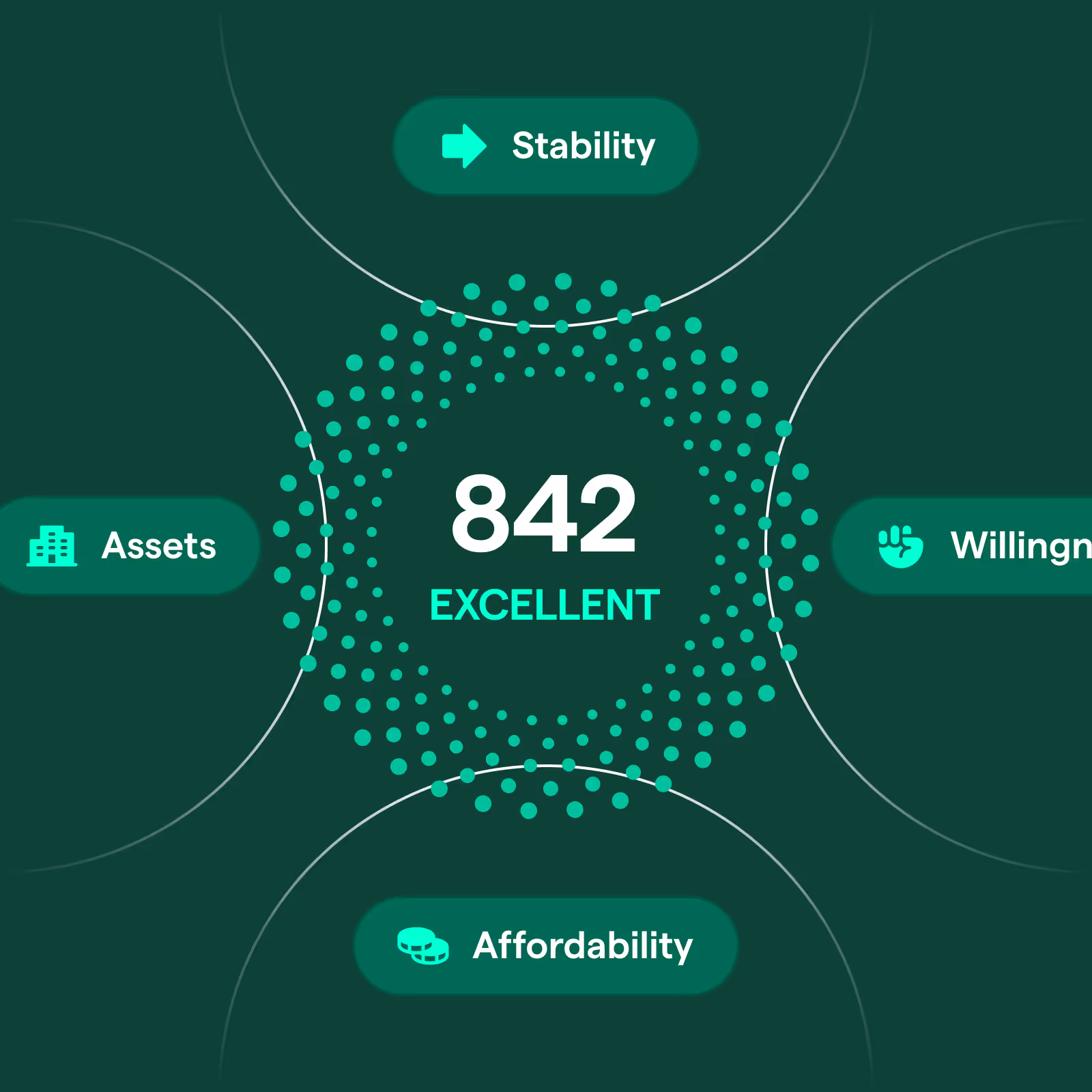

Safely Increase Credit Limits with Cashflow Scoring

Identify users who have demonstrated they can repay higher limits based on healthy cashflows across income, balances, liabilities, and more, to raise revolving credit line limits.

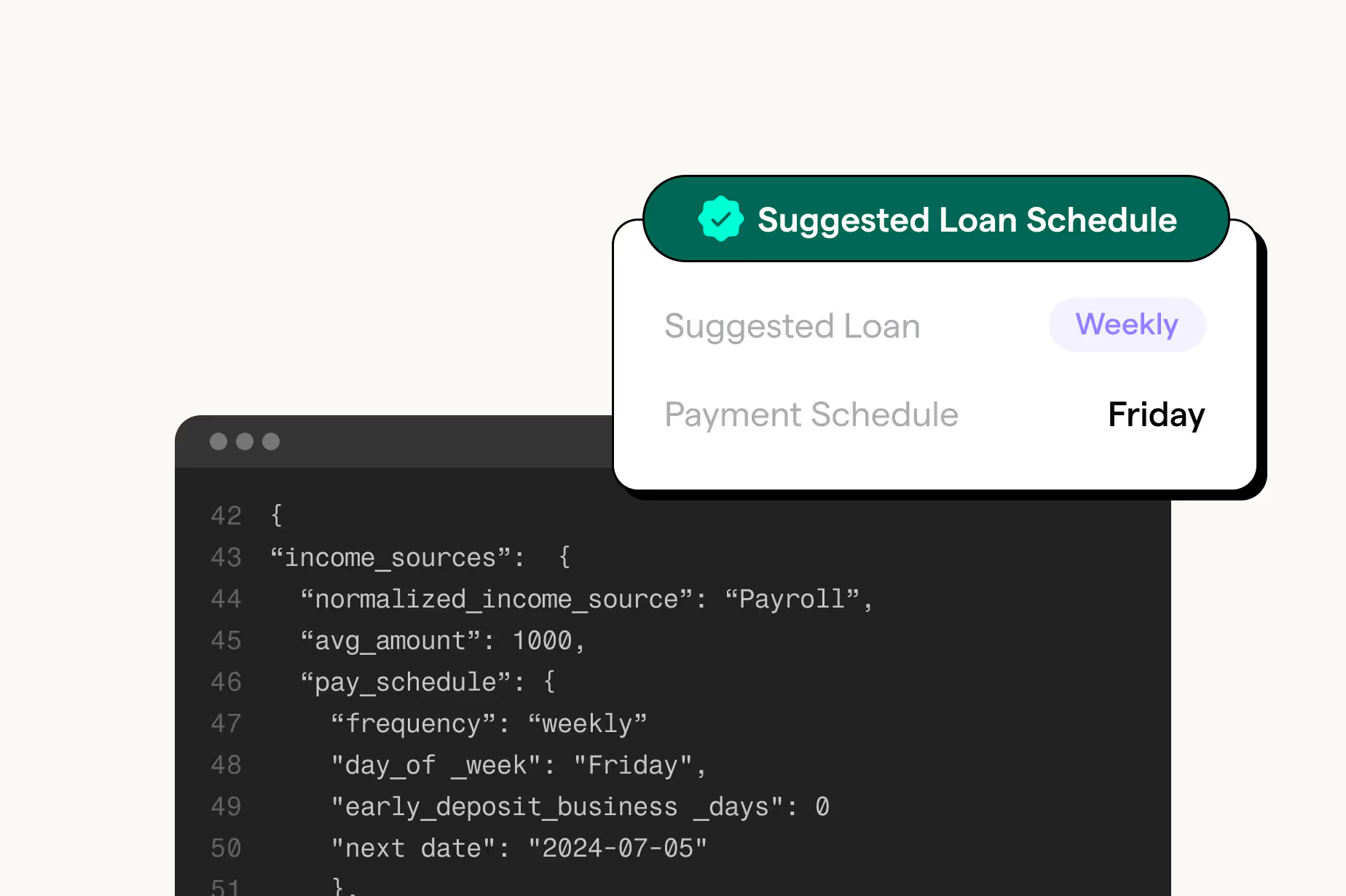

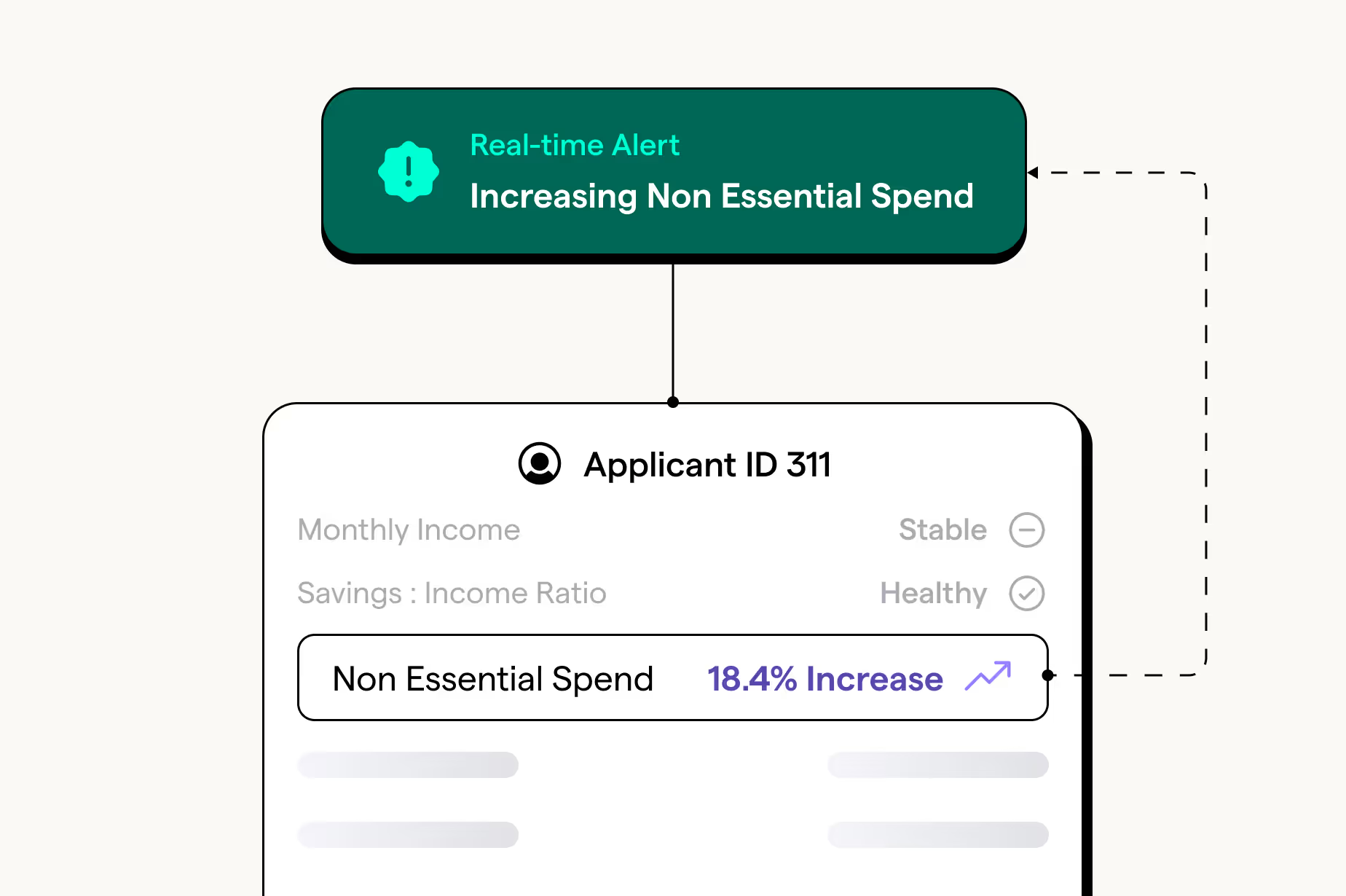

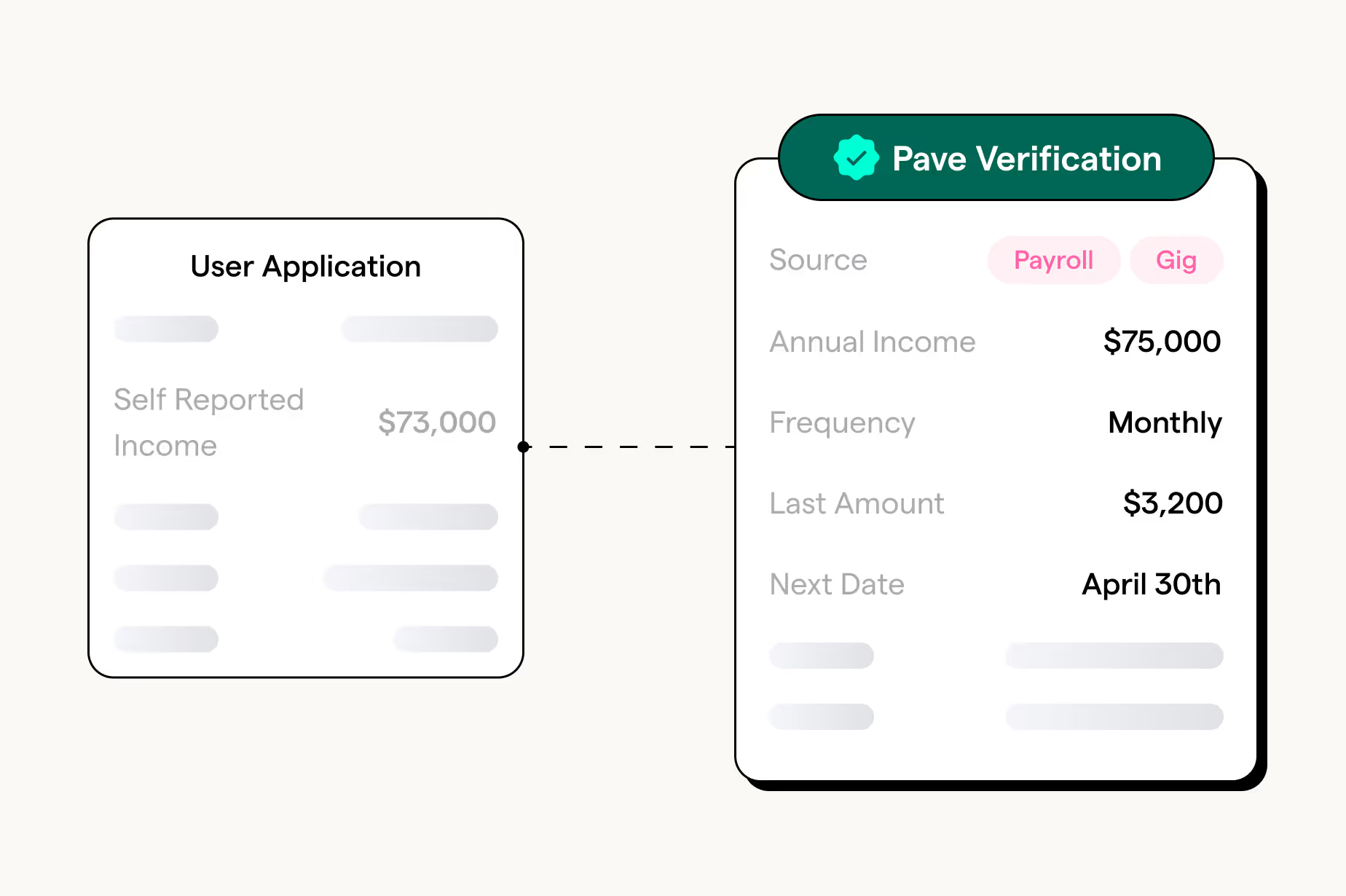

Align Payment Schedules with Cashflow Insights

Identify multiple income streams and align the scheduled payment date with when users have funds, reducing NSFs and building trust.

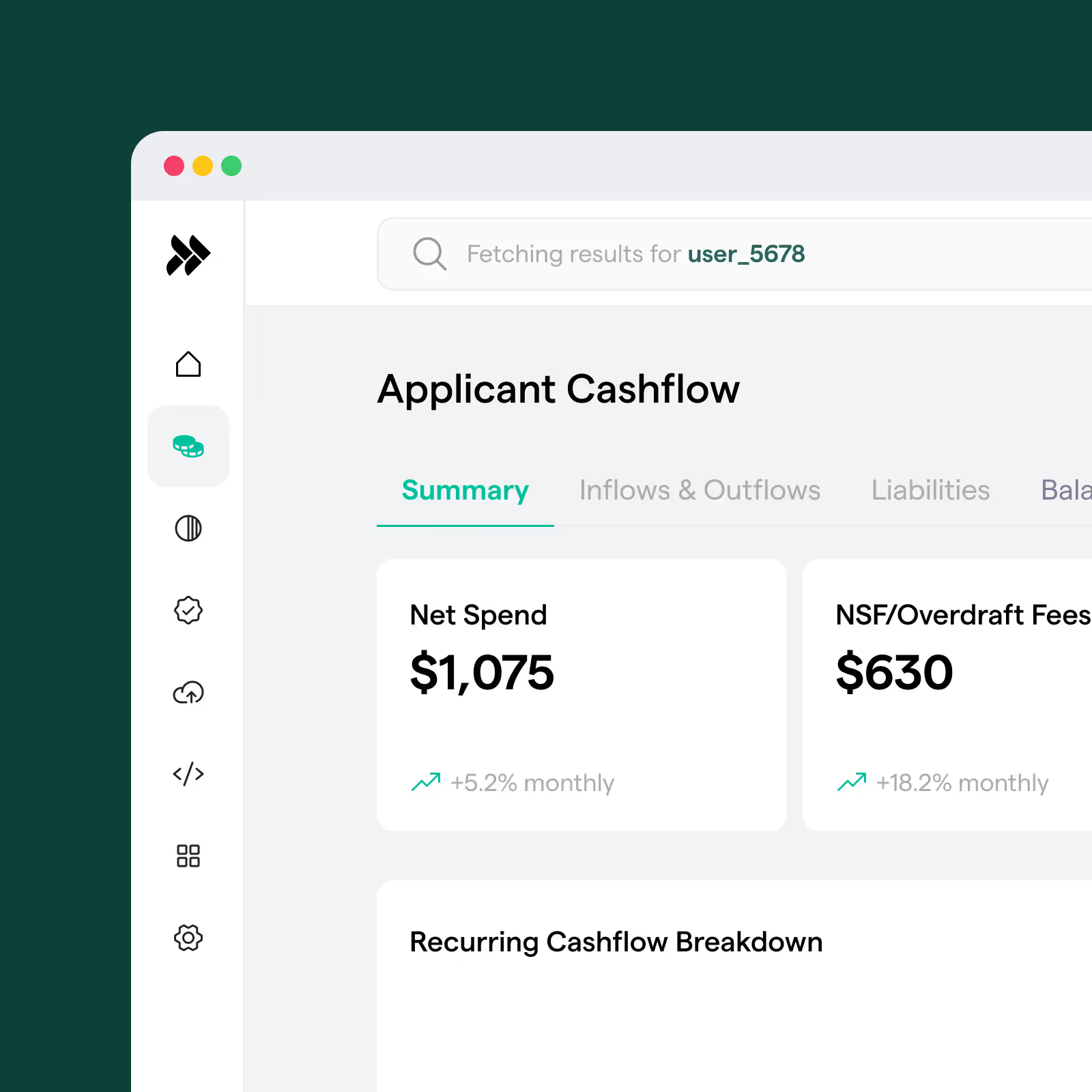

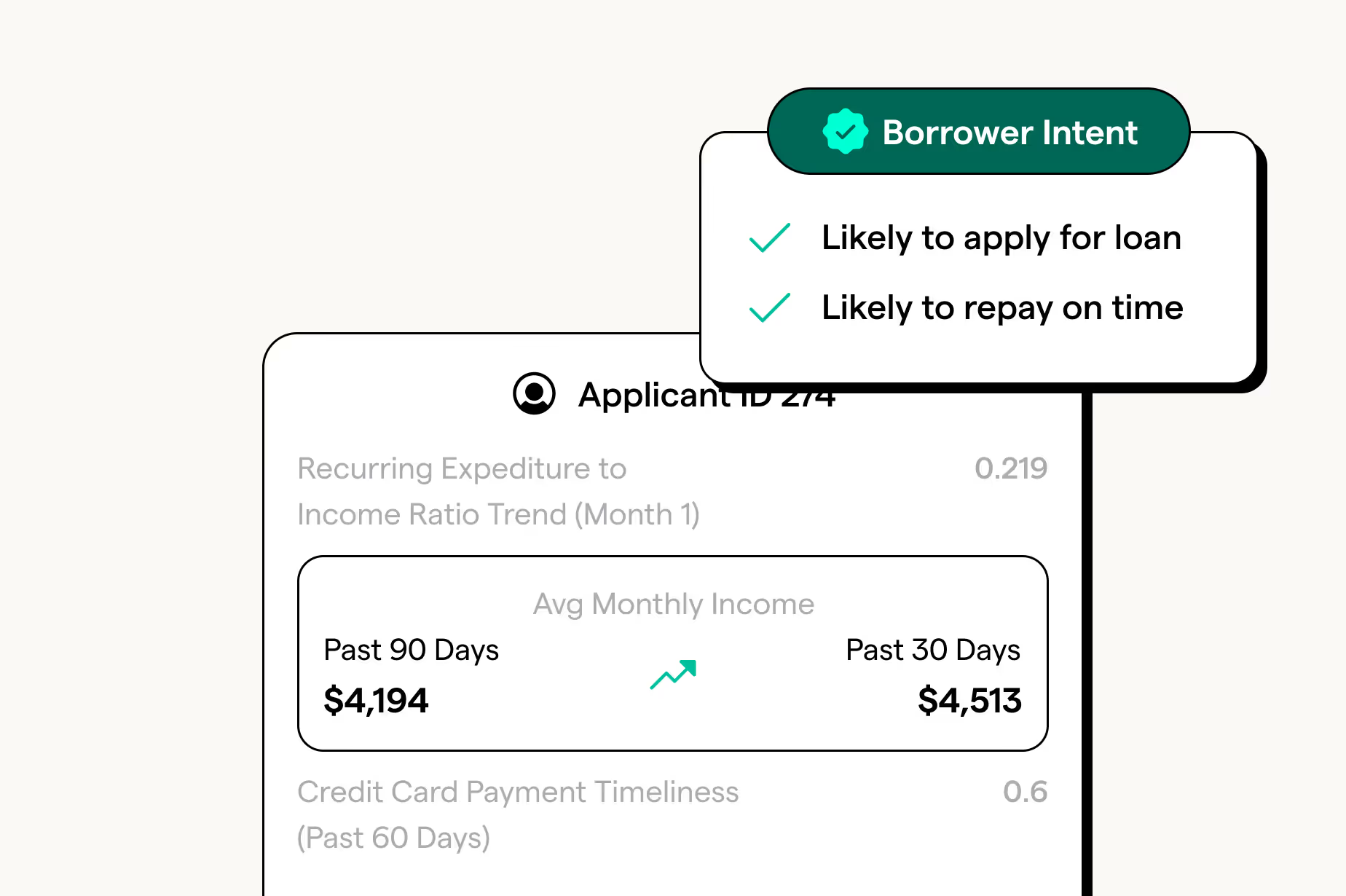

Monitor Borrower Cashflow in Real Time

Track real-time income stability, spending, and financial health to adjust loan amounts, foster growth, and proactively mitigate risks before they impact your portfolio.

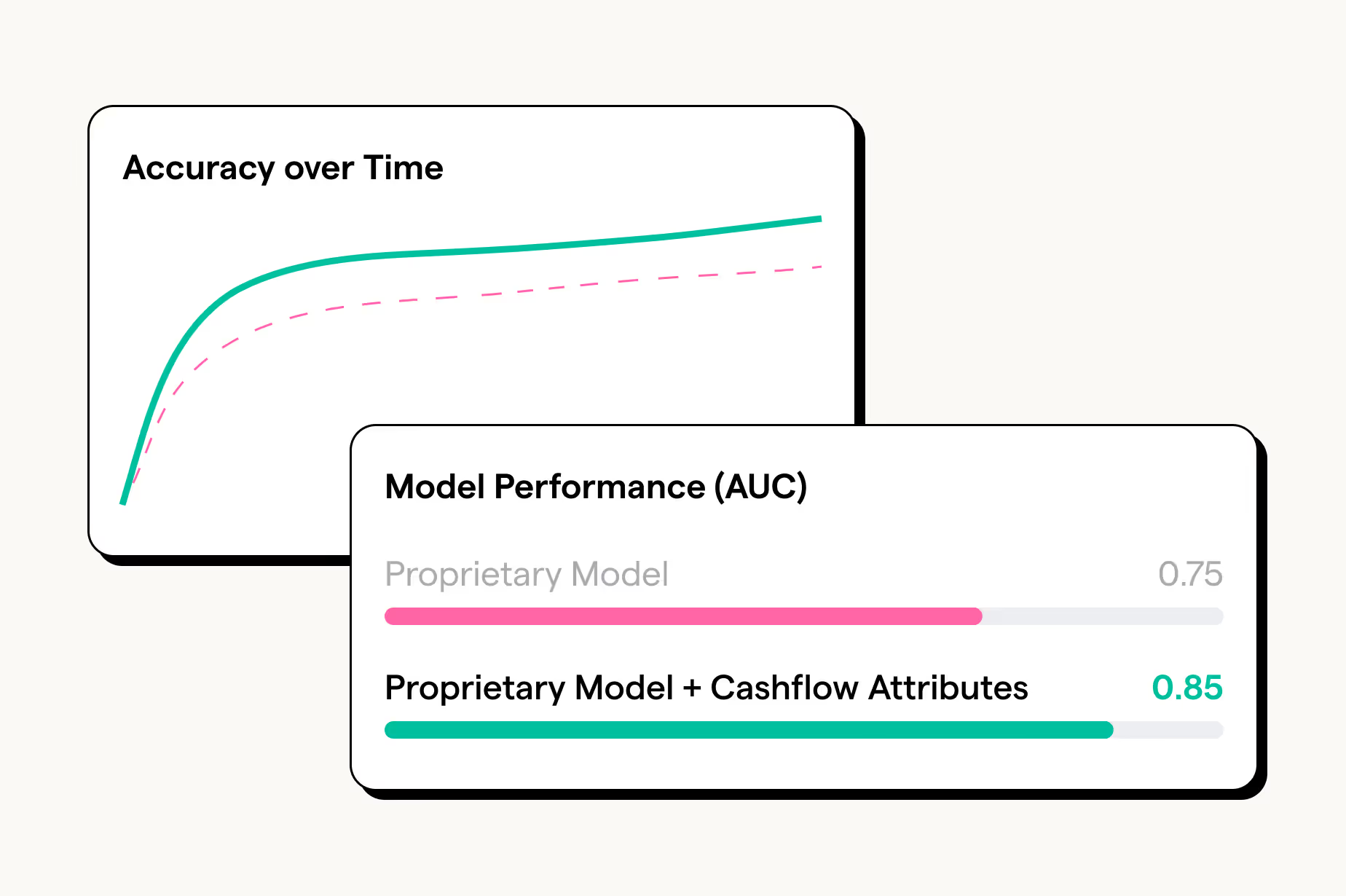

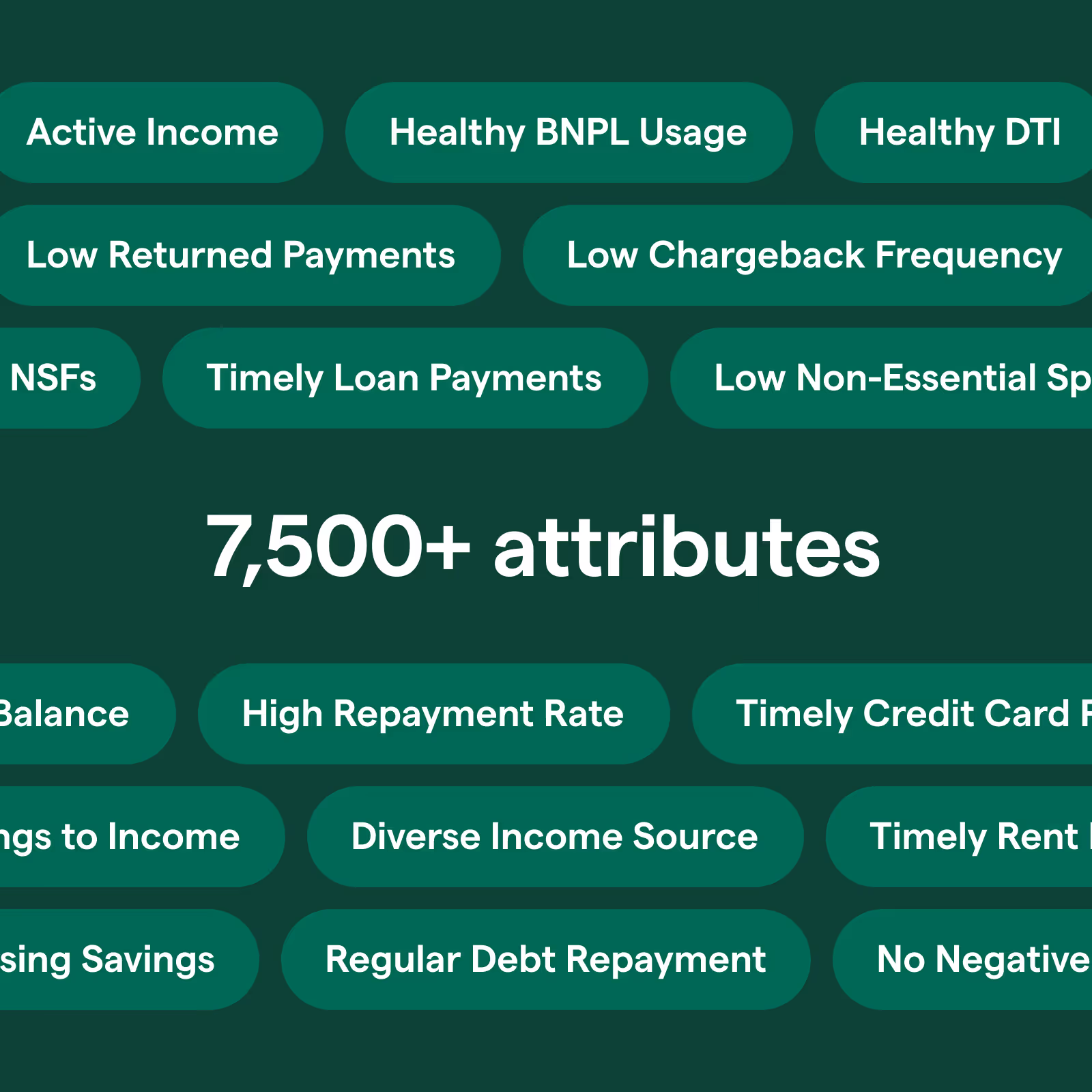

Improve Risk Models for Personal Loan Underwriting

Enhance proprietary models with Cashflow-driven Attributes and Scores to more accurately assess borrower affordability, identify healthy borrowers, and unlock new segments.

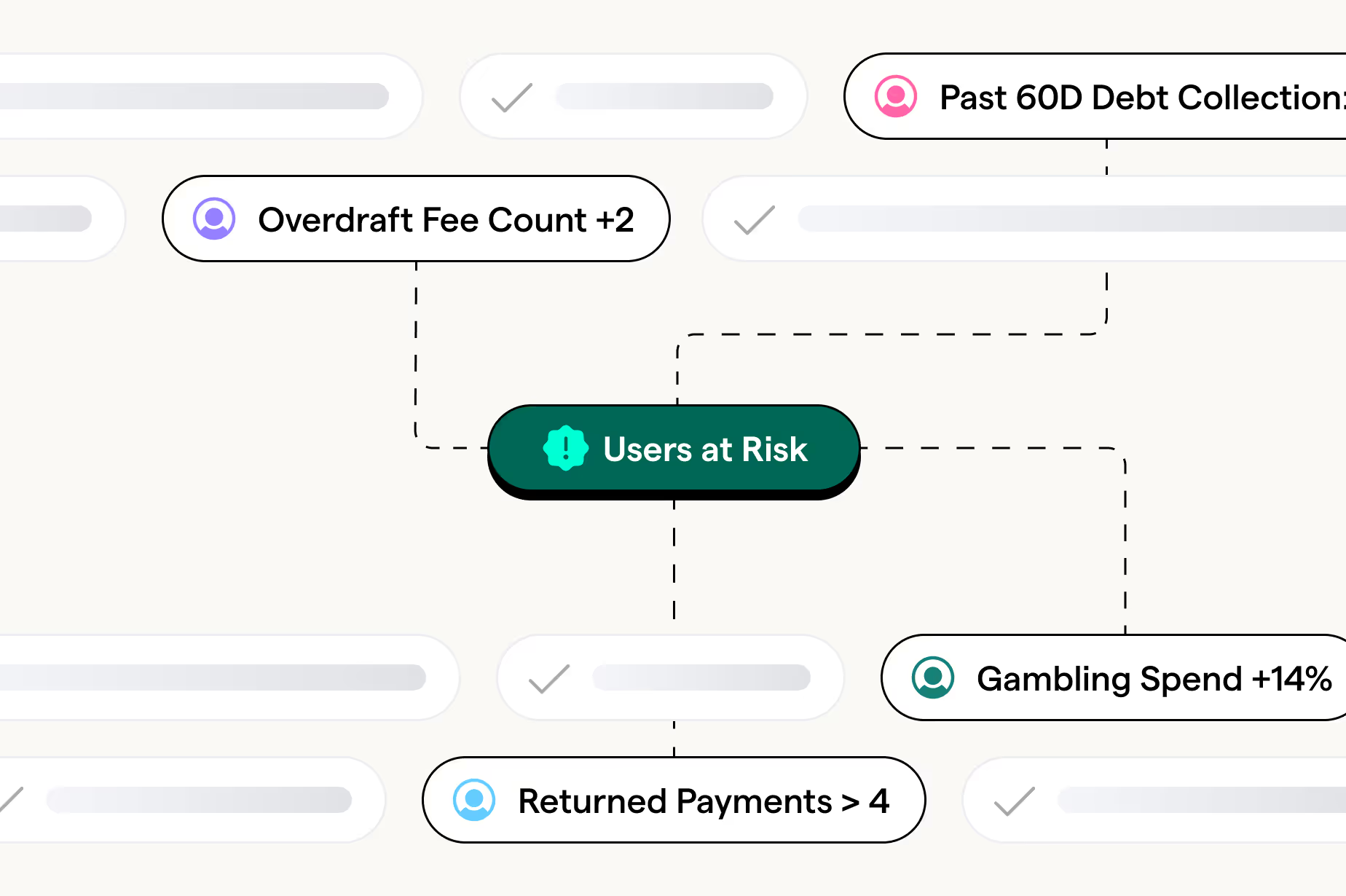

Identify Pre-Delinquency Triggers with Cashflow Signals

Surface risky behaviors from cashflow data like users falling behind on loan payments, loan stacking, and frequent chargebacks or returns.

Lower acquisition and origination costs

Strategically target existing customers demonstrating increased affordability for credit or refinancing offers.

Credit Card Underwriting FAQs

How does cashflow data improve credit card underwriting?

Cashflow data provides real-time visibility into a borrower’s income, spending patterns, and financial stability. Unlike traditional credit scores, it captures current financial behavior, allowing lenders to make more accurate and timely credit decisions.

Can cashflow-based underwriting replace traditional credit scores like FICO?

Cashflow-based underwriting is not necessarily a replacement but a powerful complement to traditional credit scores. It enhances decisioning by identifying creditworthy borrowers who may be overlooked by legacy models, especially thin-file or no-file applicants.

How can lenders increase credit card approvals without increasing risk?

By using cashflow analytics, lenders can better assess true affordability and repayment capacity. This enables higher approval rates while maintaining or even reducing default risk through more precise borrower segmentation.

What are thin-file borrowers and how can they be evaluated?

Thin-file borrowers are individuals with limited or no credit history. Cashflow data allows lenders to evaluate these applicants based on income consistency, spending behavior, and financial stability rather than relying solely on credit bureau data.

How does cashflow data help optimize credit limits?

Cashflow insights enable dynamic credit limit setting based on real income and spending capacity. This helps lenders offer appropriate limits that maximize revenue while minimizing overextension and risk.

Can cashflow analytics help detect early signs of default?

Yes. By monitoring changes in income, spending patterns, and account balances, cashflow models can identify early warning signals of financial stress, allowing lenders to take proactive risk mitigation actions.

Is cashflow underwriting compliant with regulatory requirements?

Cashflow-based decisioning can support compliance with fair lending regulations by providing more inclusive and data-driven assessments. It can reduce bias associated with traditional credit scoring models when implemented correctly.

What types of lenders benefit most from cashflow-based credit card underwriting?

Banks, credit unions, fintech lenders, BNPL providers, and cash advance platforms can all benefit. It is particularly valuable for lenders targeting underserved or emerging credit segments.

How quickly can cashflow underwriting be implemented?

Most lenders can integrate cashflow data into their decisioning workflows within weeks, depending on their infrastructure and data providers.

What results can lenders expect from using cashflow analytics?

Lenders typically see:

- higher approval rates

- improved risk segmentation

- better-performing portfolios

- increased customer lifetime value

Explore More Products

Cashflow Scores

Offer higher amounts and drive growth with our Cashflow Scores, built on Cashflow Attributes and repayment history. Increase approvals and retention by identifying healthy, underserved borrowers.

Cashflow Attributes

Drive lift in your risk models to boost approvals with thousands of pre-built attributes built on our expansive loan performance dataset.

Cashflow Analytics

Automate processes to increase approvals and serve more borrowers using Pave’s real-time Cashflow Analytics. Streamline operations and identify healthy, underserved borrowers.

Cashflow Analytics in Snowflake

Gain seamless access to cashflow data within Snowflake to enhance analysis and decision-making. Leverage Pave’s standardized tables, updated daily, to uncover insights without complex ETL.

Related Posts

.avif)

Drive growth with Cashflow-driven Analytics

Use our Cashflow-driven Attributes and Scores to provide timely, borrower-specific insights tailored to your lending criteria. Make informed decisions that enhance approval rates and loan performance.

More Use Cases

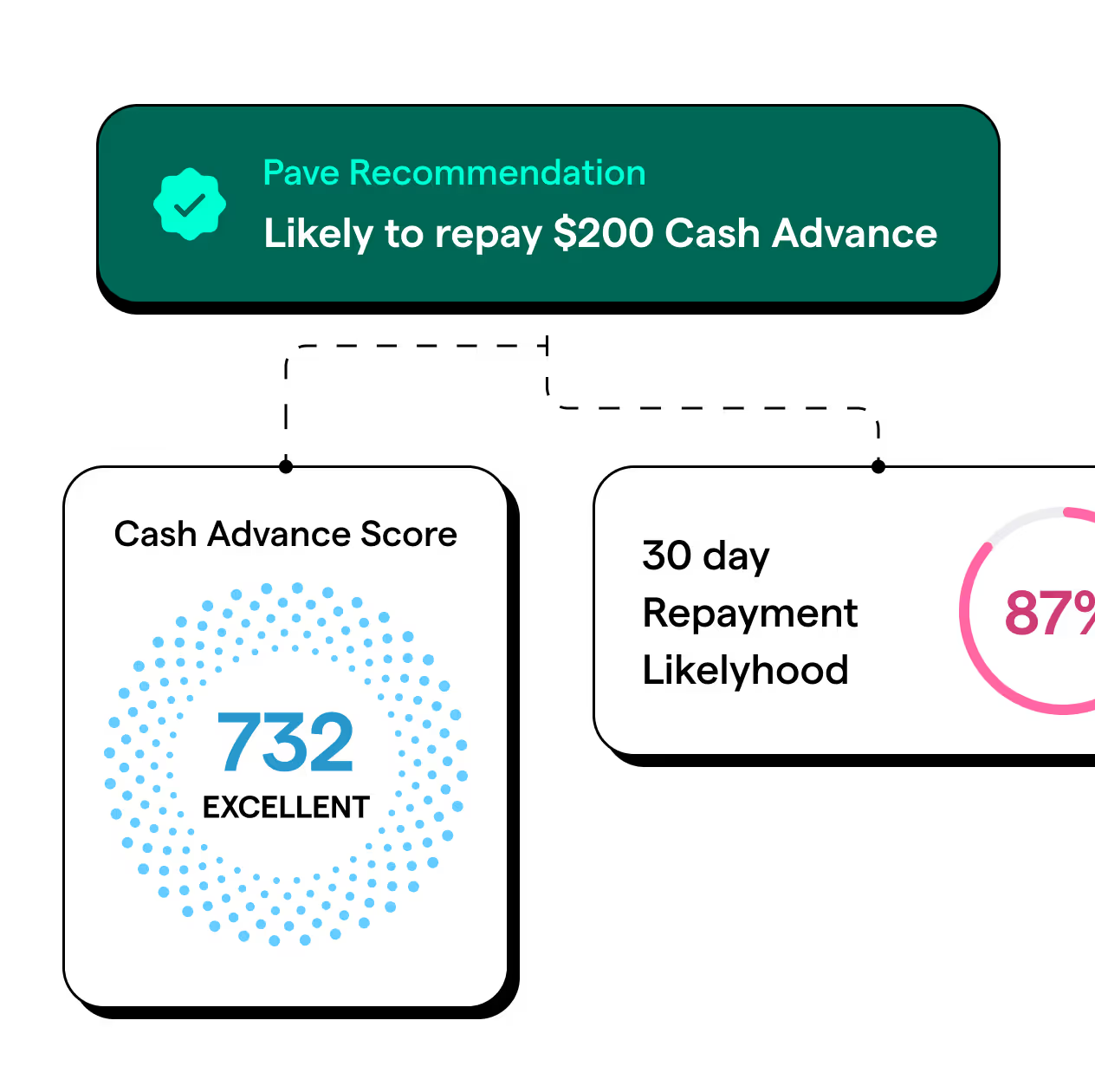

Cash Advance

Score users to increase approvals, advance amounts, and improve repayments.

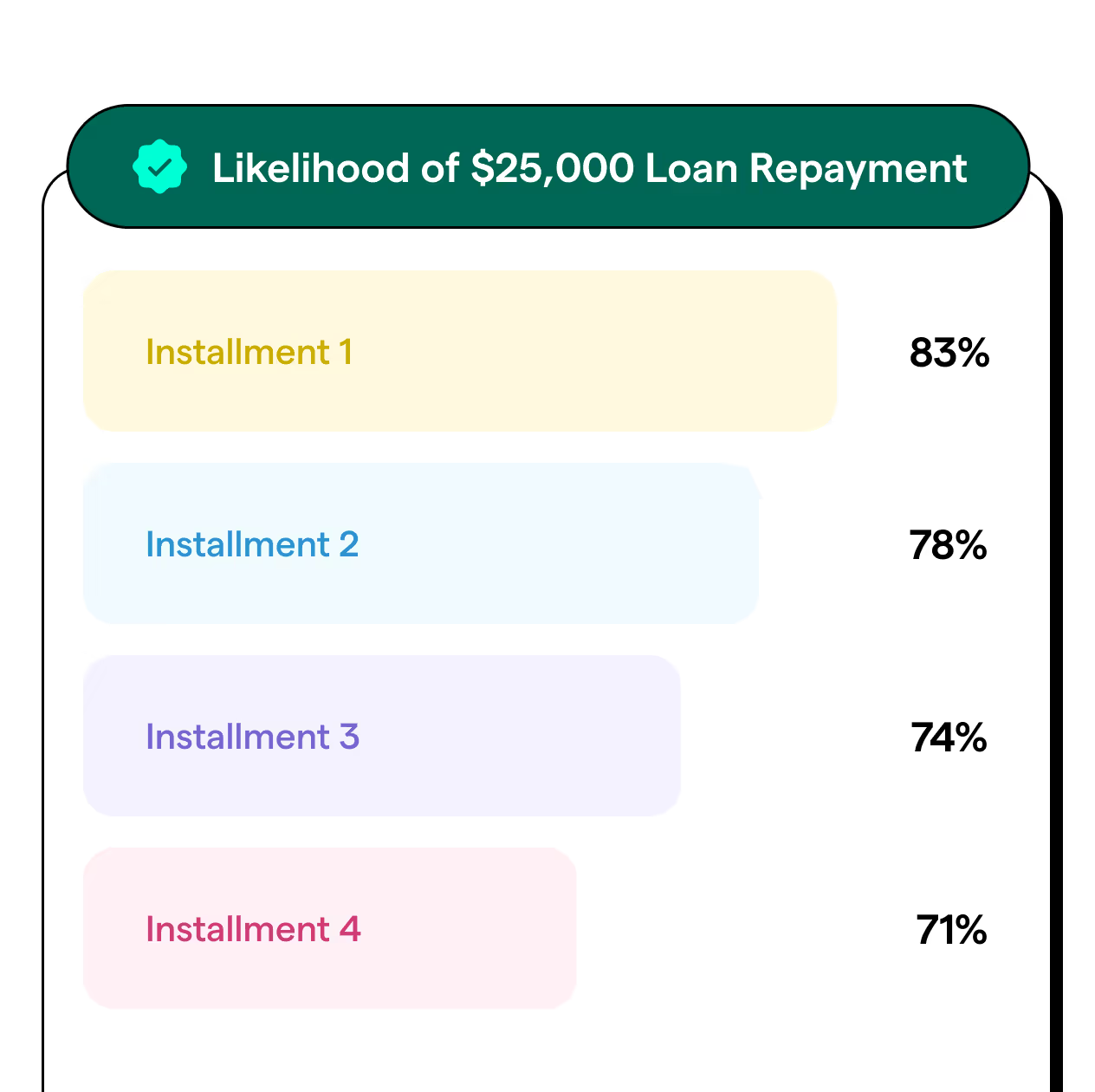

Personal Loans

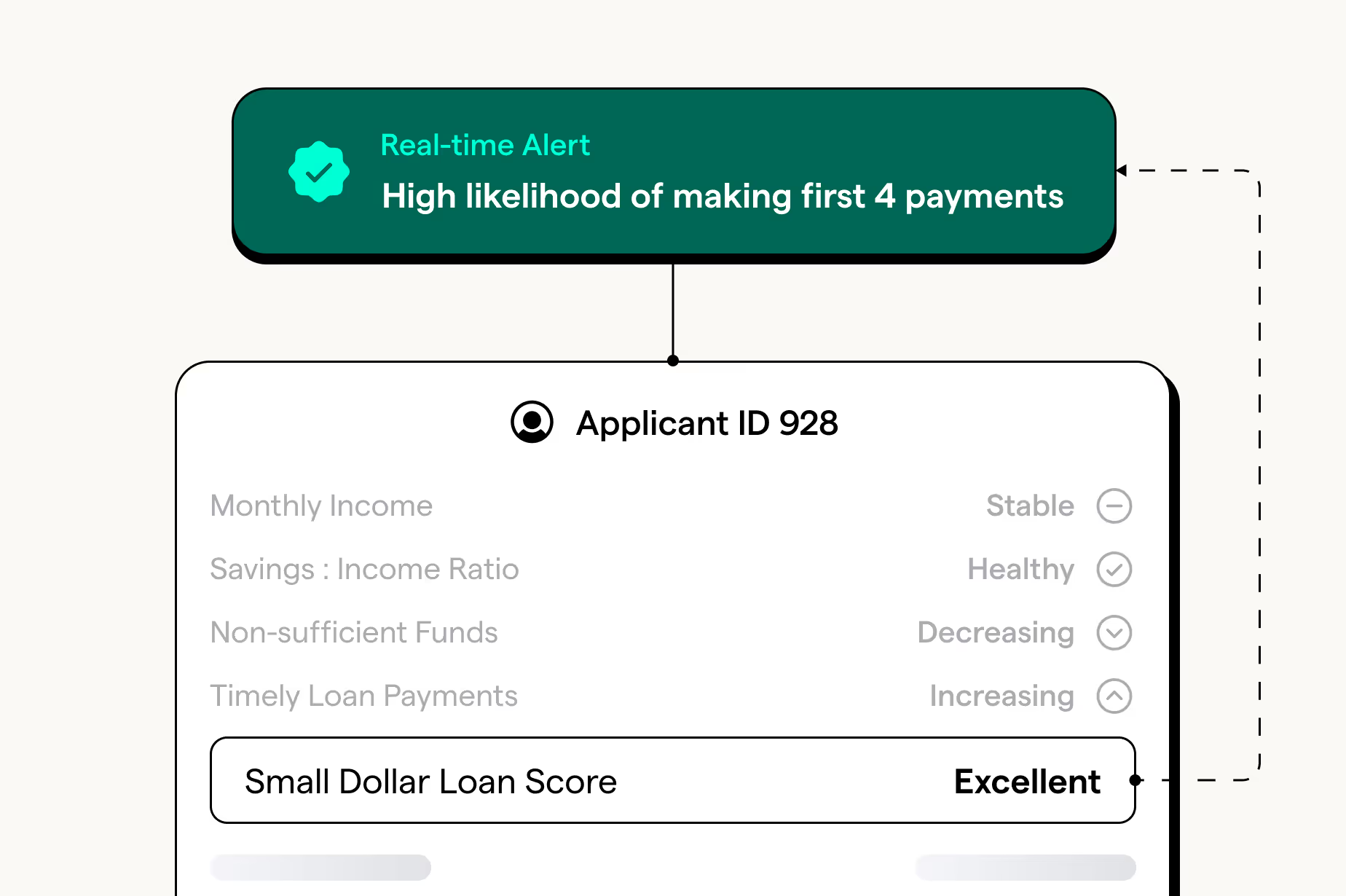

Identify users with high likelihood of making the first 4 payments to reduce delinquencies.

Small Dollar Loans

Predict repayment likelihood for the first 4 payments to reduce defaults.

Charge Cards

Graduate users to higher secured or unsecured limits based on increased affordability.