Success Stories

Real-World Case Studies from Pave Customers

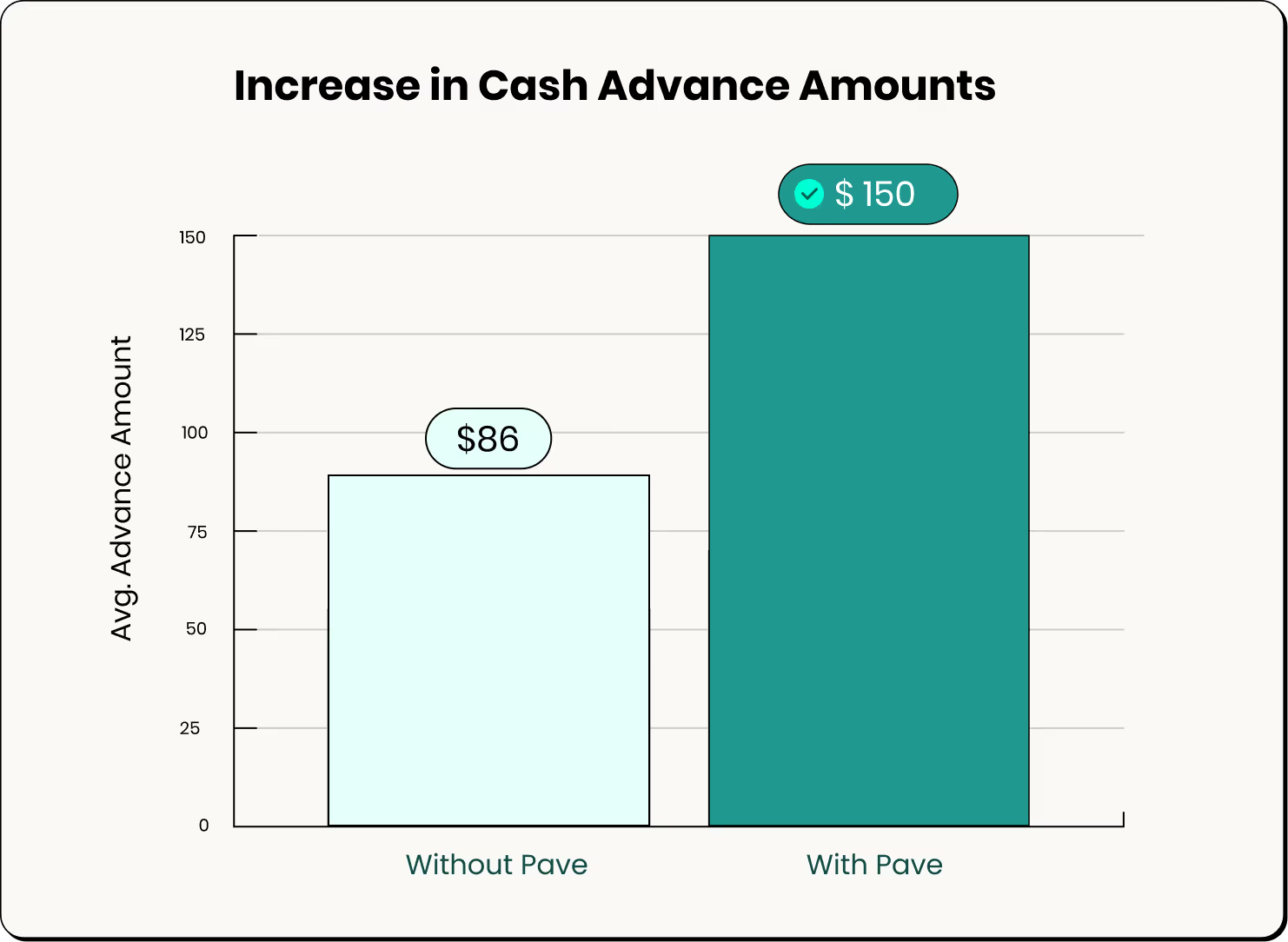

Drive growth with Cashflow-driven Analytics

Use our Cashflow-driven Attributes and Scores to provide timely, borrower-specific insights tailored to your lending criteria. Make informed decisions that enhance approval rates and loan performance.