Part 3 of the Cashflow Scoring Series

Small dollar and personal loan providers operate on tight margins and even tighter repayment windows. Whether it's a $400 emergency installment or a $5,000 near-prime loan, the underwriting challenge remains the same: predict repayment accurately, proactively, and across a diverse borrower base.

Traditional scores help sort broad risk segments, but they often fail to capture the real-time, product-specific signals that matter most in short-term lending. That’s where cashflow scores step in, giving lenders a sharper lens to evaluate both risk and opportunity based on how borrowers manage their money right now.

The Credit Gap: Who Gets Missed by Traditional Scores

Credit files offer historical views, but they often miss borrowers with real repayment potential. That includes subprime or near-prime users, immigrants, gig workers, and younger consumers, many of whom have minimal credit history, but stable financial behavior.

These users may not score well under FICO or Vantage models, but they consistently manage rent, bills, and small recurring obligations. The problem? Traditional scores weren’t built to detect short-term affordability, let alone predict repayment of an $800 installment over four weeks.

In an environment where even prime borrowers are getting declined due to tightening credit markets, lenders need better tools to unlock new segments without increasing losses.

Why Cashflow Scores Make Sense for Short-Term Credit

Cashflow scores analyze real-time bank transaction data, income streams, account volatility, repayment behavior, and liquidity buffers to give lenders a near-term view of borrower health. Instead of asking, “How does this borrower rank against the general population?” the question becomes, “How likely is this borrower to repay this specific loan starting next week?”

For small dollar and personal loans, that shift is critical. A borrower’s ability to make the first few payments is often the strongest indicator of overall repayment likelihood. And that’s exactly what a well-designed cashflow score is built to predict.

From Rank-Ordering to Outcome Predictions

Traditional credit scores are designed for broad risk sorting. Cashflow scores are designed to forecast specific, near-term repayment outcomes—such as:

- Will the borrower repay their first installment on time?

- Are they likely to complete the second and third payments without delinquency?

- Is this user showing signs of income disruption or financial stress?

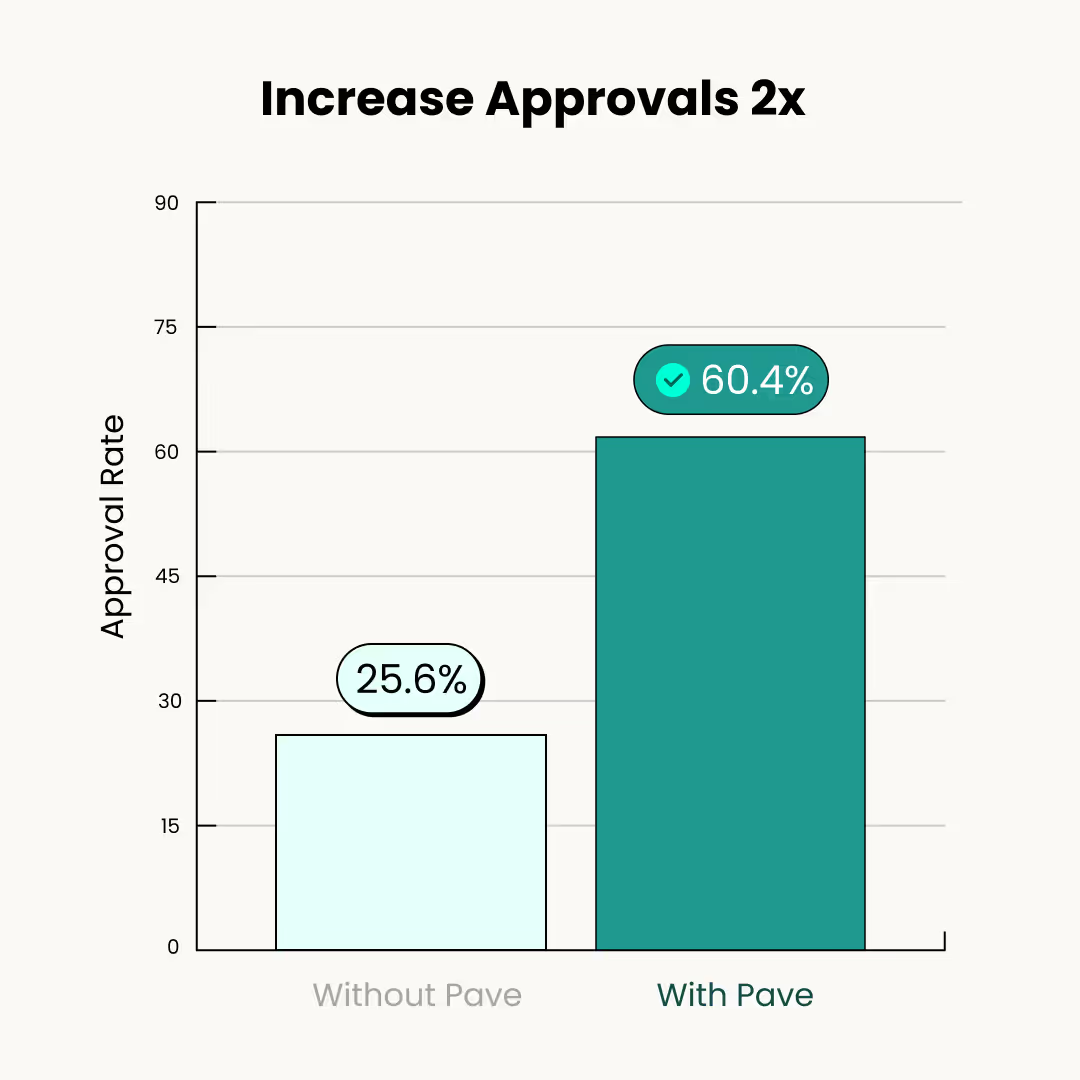

This level of granularity matters. In one case, a subprime installment lender used a cashflow-driven score to identify low-risk applicants among users previously denied under FICO-based rules. The result: approval rates increased from 25.6% to 60.4%, while reducing high-risk exposure by replacing 33% of previously approved loans.

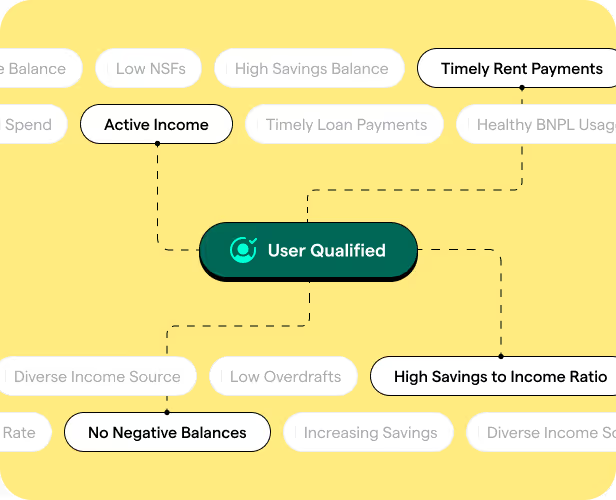

Behavioral Signals That Matter in Short-Term Lending

With cashflow scoring, it’s not just about how much a user earns. It’s about how they manage what they have and how that behavior aligns with your repayment schedule.

Key indicators include:

- Income predictability: Are paychecks regular and recurring?

- Repayment pattern: Do they already pay back other providers on time?

- Account stability: Are there recent overdrafts or returned payments?

- Liquidity buffer: How much is left after core bills are paid?

- Debt load and stacking: Are they juggling multiple short-term obligations?

These signals can be embedded directly into underwriting models to better segment risk, especially within subprime and near-prime bands, where differences in repayment behavior are often subtle but meaningful.

Aligning Decisions With Real Affordability

Many short-term loans are auto-collected. If funds aren’t available at the right time, it results in failed payments, NSF fees, and churn. Cashflow scores help align repayment schedules with actual fund availability by predicting income timing and surfacing early signs of stress.

For example, if a user gets paid weekly but a repayment is scheduled on day six, just before payday, models can flag a timing mismatch. That insight can drive proactive intervention, such as payment rescheduling or limit adjustments, without harming the user experience.

Unlocking New Segments Without Taking on More Risk

Lenders using cashflow scores can approve more borrowers who would otherwise be screened out under traditional credit rules. This includes:

- Thin-file users with limited or no credit history

- Gig economy earners with nontraditional pay schedules

- Young or immigrant consumers whose income is stable but undocumented in bureau data

At the same time, they can avoid being misled by a “good” FICO score when recent cashflow patterns — overdrafts, irregular deposits, or stacking — suggest higher risk.

The result: smarter approvals, lower delinquency, and better portfolio performance.

Faster Decisions, Less Manual Work

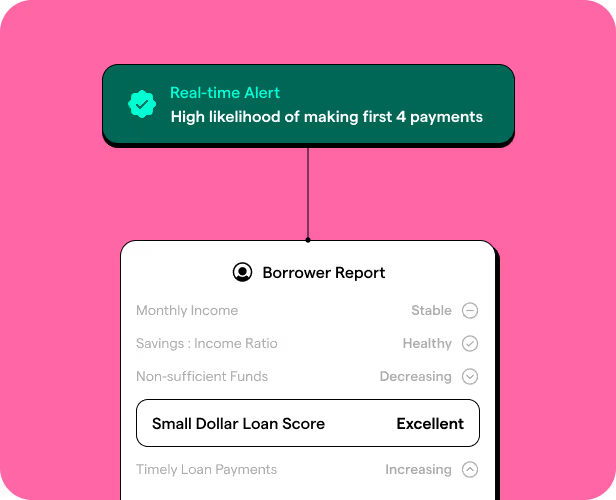

Cashflow scoring doesn’t just improve accuracy — it also cuts down on operational overhead. Risk teams no longer need to comb through raw transaction data manually. Instead, they receive over 10,000 real-time cashflow attributes — from deposit cadence to risk flags — ready to plug directly into models or decision engines.

Integration is straightforward: via API, Snowflake, or through platforms like Taktile and Effectiv. This makes it easy for teams to test, iterate, and deploy quickly. With champion/challenger setups, new models can be evaluated side-by-side with existing ones, ensuring confidence before rolling out at scale.

Why This Matters Now

Approval rates are tightening. Acquisition costs are rising. And borrowers across the spectrum are facing more volatility. For personal and small-dollar lenders, the challenge is clear: they need tools that reflect today’s borrower — not just their past.

Cashflow scores meet this need by providing a more dynamic view of affordability. They help uncover blind spots in traditional credit data and give lenders the confidence to serve a broader population without taking on unnecessary risk.

What’s Next

In Part 4, we’ll explore how cashflow scores support Credit Builder and Charge Card providers helping them set dynamic limits, reduce drop-off, and expand access to new credit users.

Want to explore how these signals would work in your own models? Book a demo to see cashflow scoring in action.