Prism is a score.

Pave is the factory that makes it.

Risk teams switch from Prism to Pave when one frozen cashflow score stops carrying eight different decisions. You keep the data feeds — we replace the model.

Drop-in replacement for the Prism score call

5-day side-by-side benchmark

You own every model

the core difference

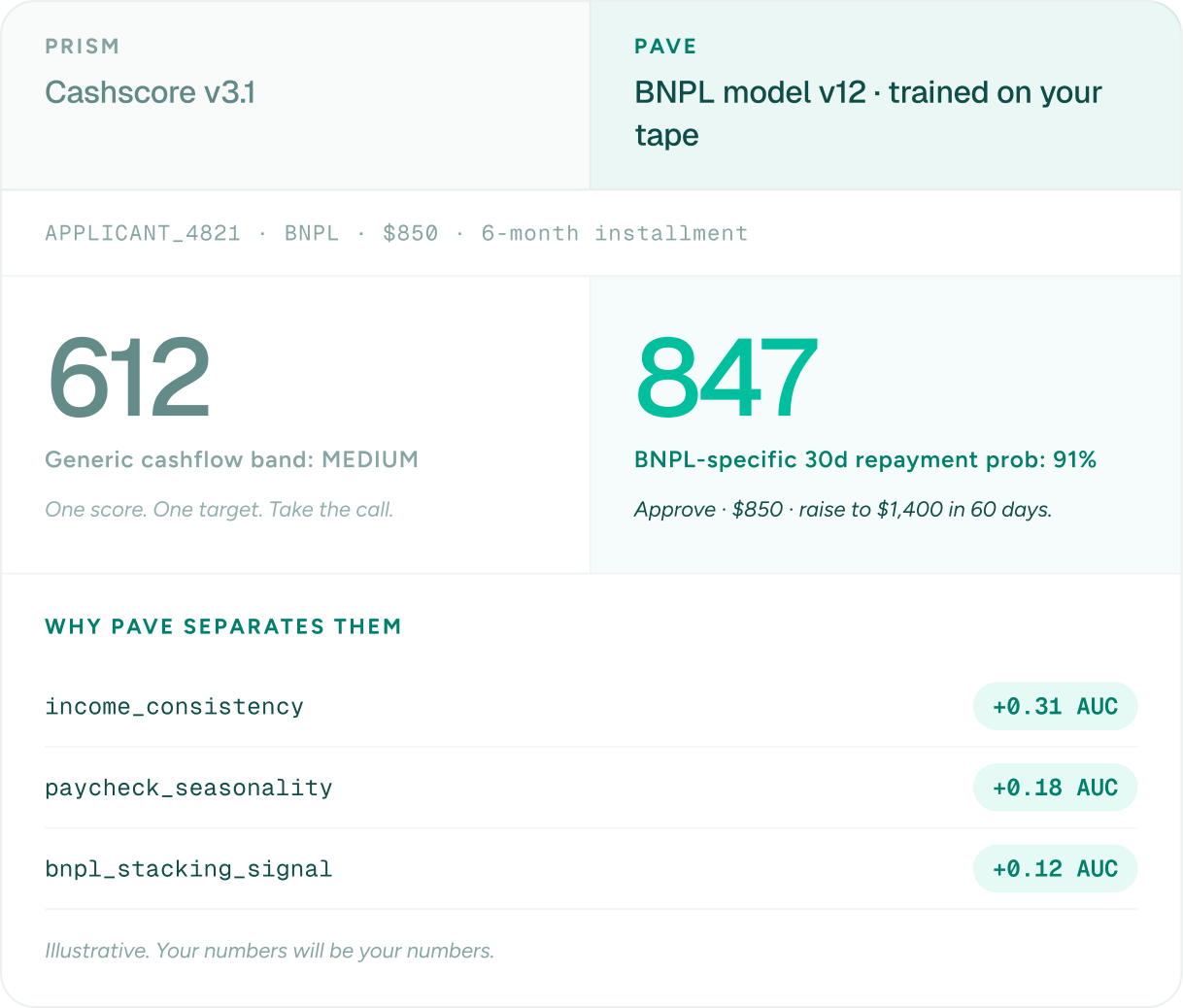

One score for everything, or a sharper model per decision.

Prism

INCUMBENT

What Prism sells today

1

One model, one target

Same Cashscore underwrites a $200 cash advance and a $20k personal loan. Same target. Same blind spots.

2

Refresh cadence: ~24 months

Major model rebuilds shipped roughly every two years. No champion-challenger. No drift dashboards.

3

Per-pull, origination-only

Priced for one decision call per applicant. Nothing built around monitoring or collections.

4

A black box you license

You take the score. You don't see the weights, the version history, or the model card.

vs

CHALLENGER

What Pave gives you instead

1

A model per decision

Approve. Limit. Pricing. Collection timing. ACH return. Each one gets its own model, trained on your tape.

2

Continuous versioning

Every model versioned, monitored for drift, and shadow-tested in production. You see what changed and why.

3

Volume contract, full lifecycle

One price. Score at origination, monitor mid-loan, retime ACH, prioritize collections — same feed.

4

Your model, your weights

Audit-ready model cards, exportable explanations, MRM artifacts. The IP sits with you.

Eight decisions, one frozen score

Prism answers one question. Your risk team makes eight.

For every decision after origination, the Cashscore was trained against the wrong target. Here's where Pave plugs in.

Decision

Target it should optimize

PAVE

Prism

Underwrite

Default risk

Set credit limit

Loss-adj. revenue

Price the loan

Expected return

Line expansion

Incremental risk

ACH timing

Return-on-debit risk

Portfolio monitoring

Roll-rate signal

Collection priority

Recoverable balance

Re-up offer

90d retention risk

WEDGE

A single Cashscore was enough when one model carried one decision. The moment your team is making eight, a model tuned to each one pulls more from the same data: in one head-to-head backtest, a lender scoring against its own outcomes cut losses by roughly half while doubling revenue versus its incumbent cashflow score.

Migration

What switching from Prism actually looks like.

You don't rip out a credit model on day one. Here's the six-step path most teams take — shadow first, ramp second, retire third.

1

Day 0

Send a deidentified loan tape

A few thousand applications with their Prism score and 30/60/90 outcomes is enough to start.

2

Days 1–3

We score it against your incumbent

Pave runs your tape through a per-product model and compares lift vs. the Prism Cashscore on the same applicants.

3

Day 5

You get a side-by-side report

AUC, KS, gini per cohort. Approval rate at fixed loss. Loss at fixed approval rate. Population separation by decile.

4

Week 2

Shadow Pave alongside Prism

Same API contract. Your decisioning code keeps calling Prism while we mirror every call. Zero traffic change.

5

Week 6

Switch on champion-challenger

10% of traffic on Pave, 90% on Prism. Watch the lift. Ramp at your comfort.

6

Week 12

Retire the Prism contract

Most lenders are 100% on Pave by week 10. We help draft the wind-down notice.

The honest answers to the hard questions.

Pave ships the same MRM artifacts Prism does — model card, validation report, fair-lending tests, monitoring plan — plus the underlying weights and feature importances. Most MRM reviews of Pave finish in 3–4 weeks because there's more documentation, not less.

Pave has been live in production with lenders since 2021 across BNPL, cash advance, small-dollar, and consumer installment. Reference calls available with risk teams who switched off Prism specifically.

Same API contract. Pave runs in shadow first while Prism stays in the decisioning path. Zero traffic change until you flip a feature flag.

We score them against Pave's taxonomy on day one and tell you which ones still earn their slot in the model. Most teams keep 30–50% of their existing feature library.

Pave's lift over Prism is largest on thin-file: gig income, irregular pay cycles, sub-12-month history. That's the segment where one frozen score has the least to say.

No per-pull pricing. You get a volume-based contract that lets you score at origination, mid-loan, and pre-ACH without three line items. Most lenders see net savings vs. Prism within 90 days.

Run the Prism head-to-head

Bring your Cashscores. We’ll show you the lift.

Send a deidentified loan tape and get back a full Pave vs. Prism lift report—model accuracy, approval rate delta, and disparity outcomes.

Results in 5 business days

SOC 2 Type II

Your Prism contract stays in place