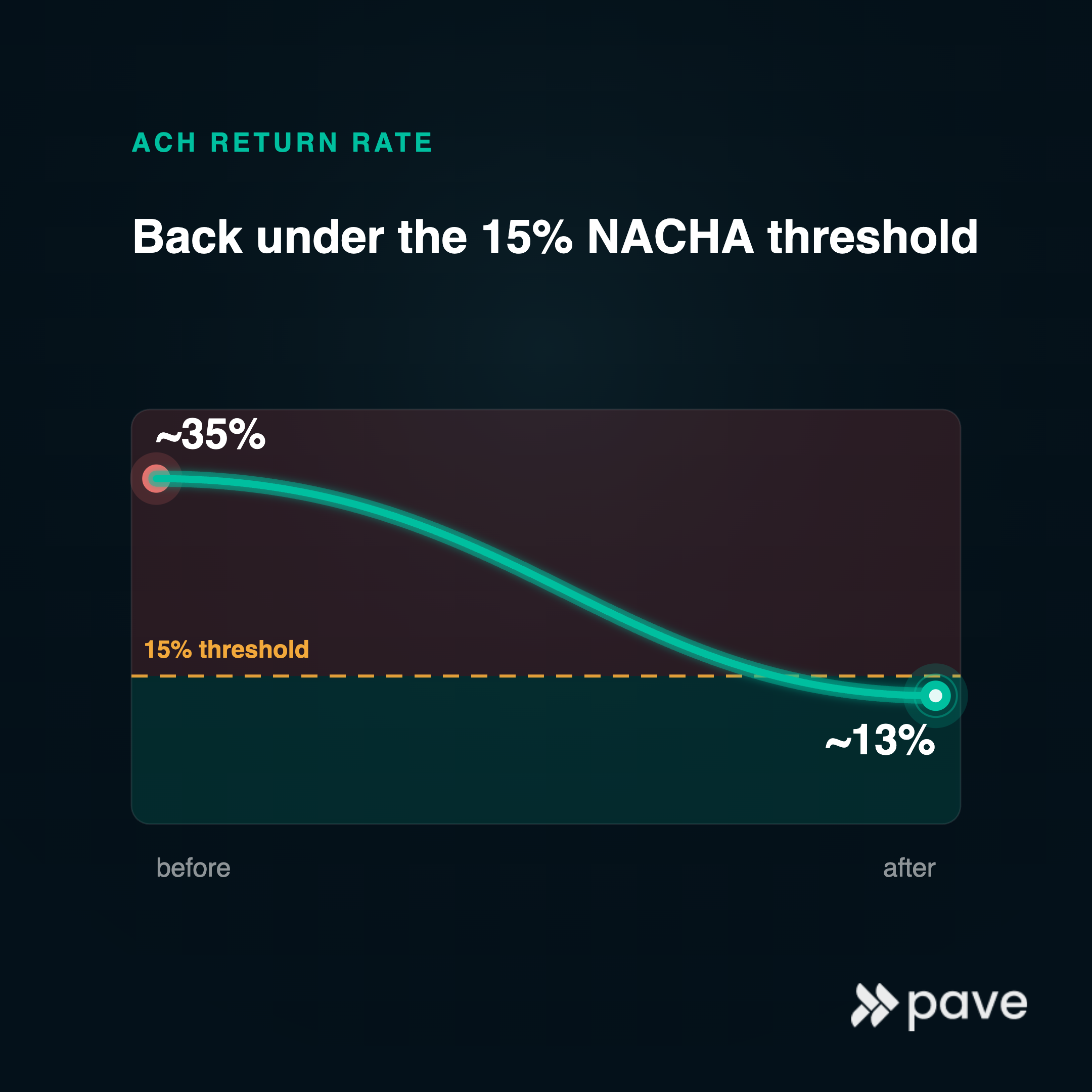

How an earned wage access provider cut ACH returns from 35% → 13% to get back under NACHA threshold

A balance check on every retry wasn't working, and it was costly.

Challenge

The provider's ACH return rate had climbed past 35% — more than 2x NACHA's 15% threshold. Sustained breaches get a lender's access to the ACH rail revoked. For an earned wage access business, losing the ACH rail isn't a setback, it's an extinction event.

The team had been running an ODFI passthrough balance check on every retry. If the account showed sufficient funds at the moment of submission, the retry went through. The check worked for the obvious cases. But it missed something subtler: a momentary balance doesn't predict whether the money will still be there when the ACH actually settles. A user who has $300 in the account at 2pm and zero by 11pm looks fundable at submission, but isn't. The balance check was also expensive to run on every retry, and it carried a downstream cost the provider felt directly. When a retry landed against an account whose balance had since evaporated, it pushed the user into overdraft, generating fees the provider was effectively causing its own customers.

The team needed a score that could read the rhythm of repayment behavior — not just the snapshot — and operating points they could tune separately for due-date submissions and overdue retries, because the two carry materially different risk.

Solution

The team deployed Pave’s ACH Risk Score with a two-threshold design: 0.85 for due-date attempts and 0.65 for overdue retries. The two cutoffs capture a distinction a single global threshold can’t - due-date submissions ride the user’s expected paycheck rhythm, while overdue retries run against a user who has already missed. The same risk tolerance shouldn’t apply to both.

The score replaced the balance check as the decision logic on the retry path, eliminating the live balance check along with its per-retry cost and the overdraft fees that came from retrying against stale funds; the integration was a configuration change, not a new pipeline.

Approach

- Train on the provider’s own ACH retry data. Pave’s ACH Risk Score validated at AUC 0.836 in production against the provider’s prior balance-check baseline.

- Tune thresholds by attempt type. The teams analyzed the risk distribution separately for due-date and overdue retries. The 0.85 / 0.65 split came from that analysis.

- Deploy with continuous monitoring. The score went live with monitoring on return rate, AUC, and population mix.

- Re-tune as the population shifts. Through 2026, the new-user mix in the portfolio grew from ~20% to ~55%. The team re-tuned thresholds as the underlying distribution moved, keeping under the compliance threshold.

Results

- ACH return rate more than halved, from ~35% to ~13%, back under NACHA's 15% threshold.

- Collection success rose from 81.2% to 91.9%, so reducing returns didn't come at the cost of recovery.

- The top-risk decile captured 49.3% of all returns (4.3× baseline), giving operations a precise lever for the riskiest retries.

What these numbers prove together: the operator can stay under NACHA without throttling their business. The two-threshold design gave the team something a single global cutoff couldn't — an operational handle that recognizes due-date and overdue retries as different problems and lets the team manage them as such.

Conclusion

NACHA threshold management isn’t a one-time fix. The population mix in an earned wage access portfolio shifts as the business grows. A static rule deployed once will drift out of compliance with changes in new-user concentration and repayment patterns.

The advantage of running a model is the levers. By making thresholds tunable by attempt type, the operator kept compliance margin intact through portfolio change without rebuilding the underwriting stack. The provider isn’t done tuning. That’s not a flaw in the deployment, but the right operating model for the rail.

Explore Use Cases

Cash Advance

Score users to increase approvals, advance amounts, and improve repayments.

Personal Loans

Identify users with high likelihood of making the first 4 payments to reduce delinquencies.

Charge Cards

Graduate users to higher secured or unsecured limits based on increased affordability.

Credit Cards

Set dynamic credit limits based on users' income and affordability.

Drive growth with Cashflow-driven Analytics

Use our Cashflow-driven Attributes and Scores to provide timely, borrower-specific insights tailored to your lending criteria. Make informed decisions that enhance approval rates and loan performance.