Fizz Expands Approvals With Pave’s Credit Card Score

Discover how Fizz boosted credit card approvals while controlling delinquencies by using Pave’s Credit Card Score for thin-file and new-to-credit users.

Challenge

Fizz’s internal models were beginning to plateau despite analysis suggesting that there was room to improve approval rates. Given that Fizz’s core customer base is comprised of students and young adults with limited or no credit history, Fizz needed a solution that would provide net new insight into its applicant pool, and in particular its core applicant base, in order for Fizz to confidently boost approval rates in a manner that didn’t spike delinquency.

Approach

Pave partnered closely with the Fizz’s risk and data teams to establish clear thresholds, user segments, and evaluation criteria tailored for thin-file applicants. By integrating Pave’s Credit Card Score and Cashflow-driven Attributes into the Fizz’s framework, the teams added meaningful visibility where credit history was limited. Trained on billions of transactions and cross-provider performance data, Pave’s models surfaced new signals that their internal models did not previously capture.

To validate the predictive power of Pave’s models, the teams backtested the Credit Card Score and Attributes using historical bank transaction, underwriting, and collections data, benchmarking results against the Fizz’s internal models. In parallel, they developed decline reasons mapped directly to the score. This ensured transparency and compliance while equipping internal teams with clear explanations and giving declined applicants actionable feedback to improve future eligibility.

Results

Working with Pave, Fizz identified score thresholds that expanded approvals while keeping the increase in delinquency within expected, manageable levels. By incorporating these thresholds into their underwriting models, Fizz approved more qualified applicants with a tightly monitored increase in delinquencies, resulting in a positive increase in economics.

"Pave’s Credit Card Score gave us the insight and confidence to approve additional qualified applicants while still controlling for risk. By integrating Pave’s features into our underwriting models, we gained new insight into repayment risk specific to our product and have been able to adapt in real time as our users’ financial health changes. It’s helped us grow faster and smarter.”

— Carlo Köbe, Co-Founder & CEO of Fizz

Fizz’s underwriting model became significantly better at distinguishing between applicants who repay and those who default, evidenced by a double-digit lift in model predictive power for thin-file users. In addition, Fizz introduced clear, data-backed decline reasons tied to Pave’s attributes. This gave internal teams greater visibility into decisions and Fizz declined applicants with actionable guidance to improve future eligibility.

Together, these changes allowed Fizz to segment risk with more precision, approve more qualified applicants, and achieve sustainable portfolio growth powered by insights beyond traditional credit data.

Conclusion

By delivering transparent, data-backed rejection reasons and improving decisions for thin-file applicants, Fizz unlocked new opportunities for safe growth. These results validated Pave’s Credit Card Score as a powerful and explainable complement to their existing risk strategies.

Teams leverage Pave’s Credit Card Score in their proprietary models to increase approvals without increasing risk. Read more about our Cashflow Scores or book a demo.

Explore Use Cases

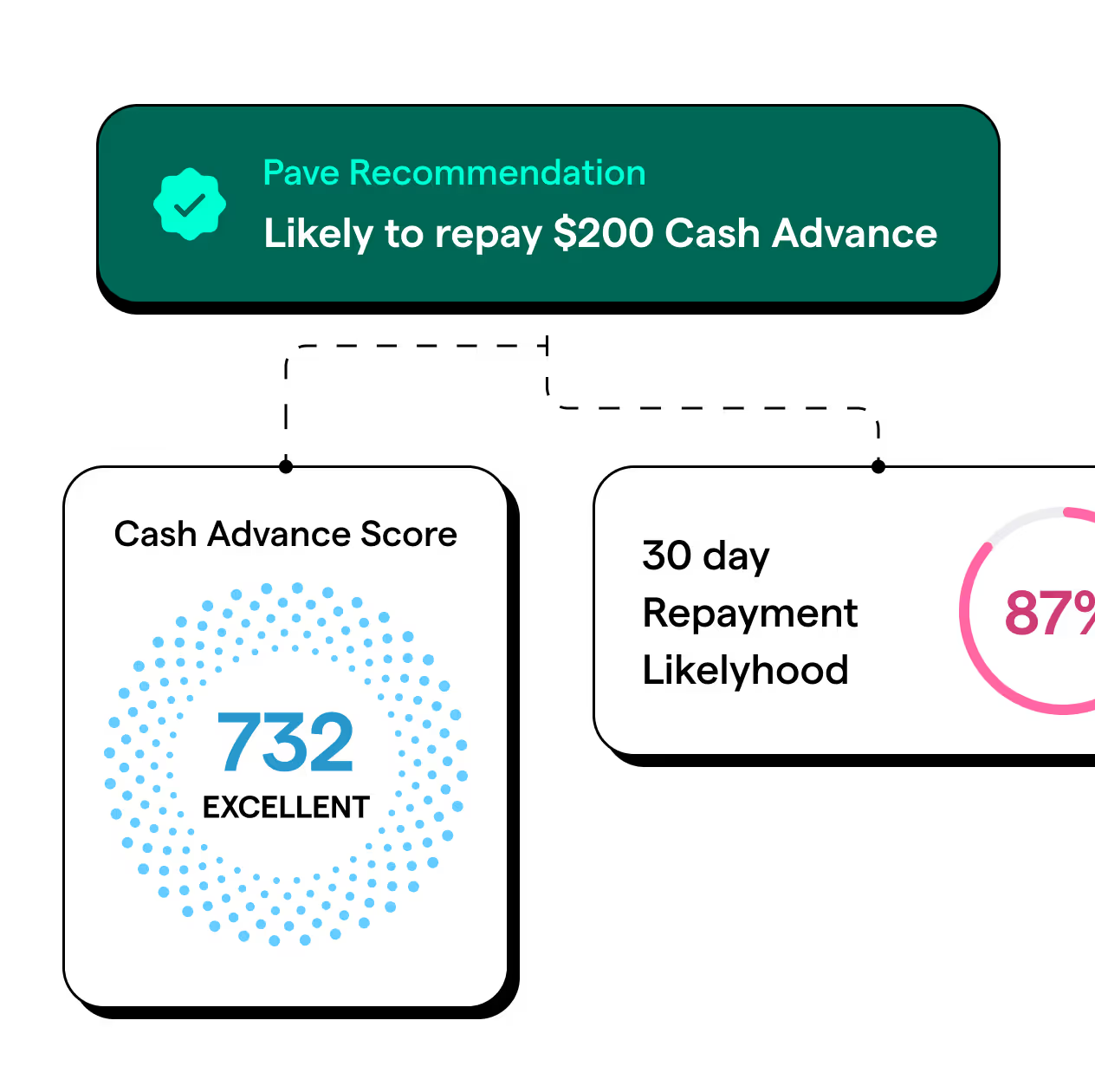

Cash Advance

Score users to increase approvals, advance amounts, and improve repayments.

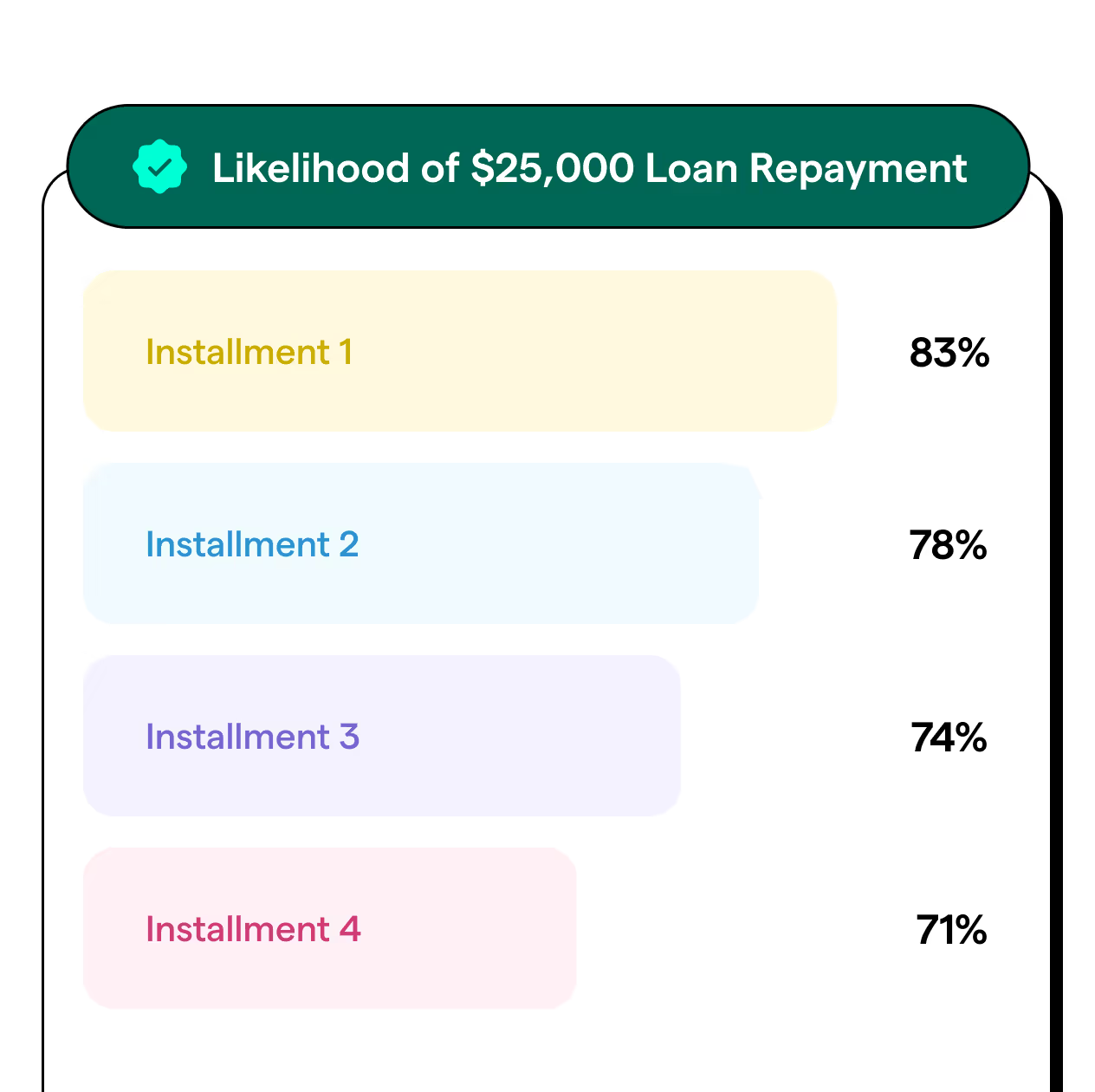

Personal Loans

Identify users with high likelihood of making the first 4 payments to reduce delinquencies.

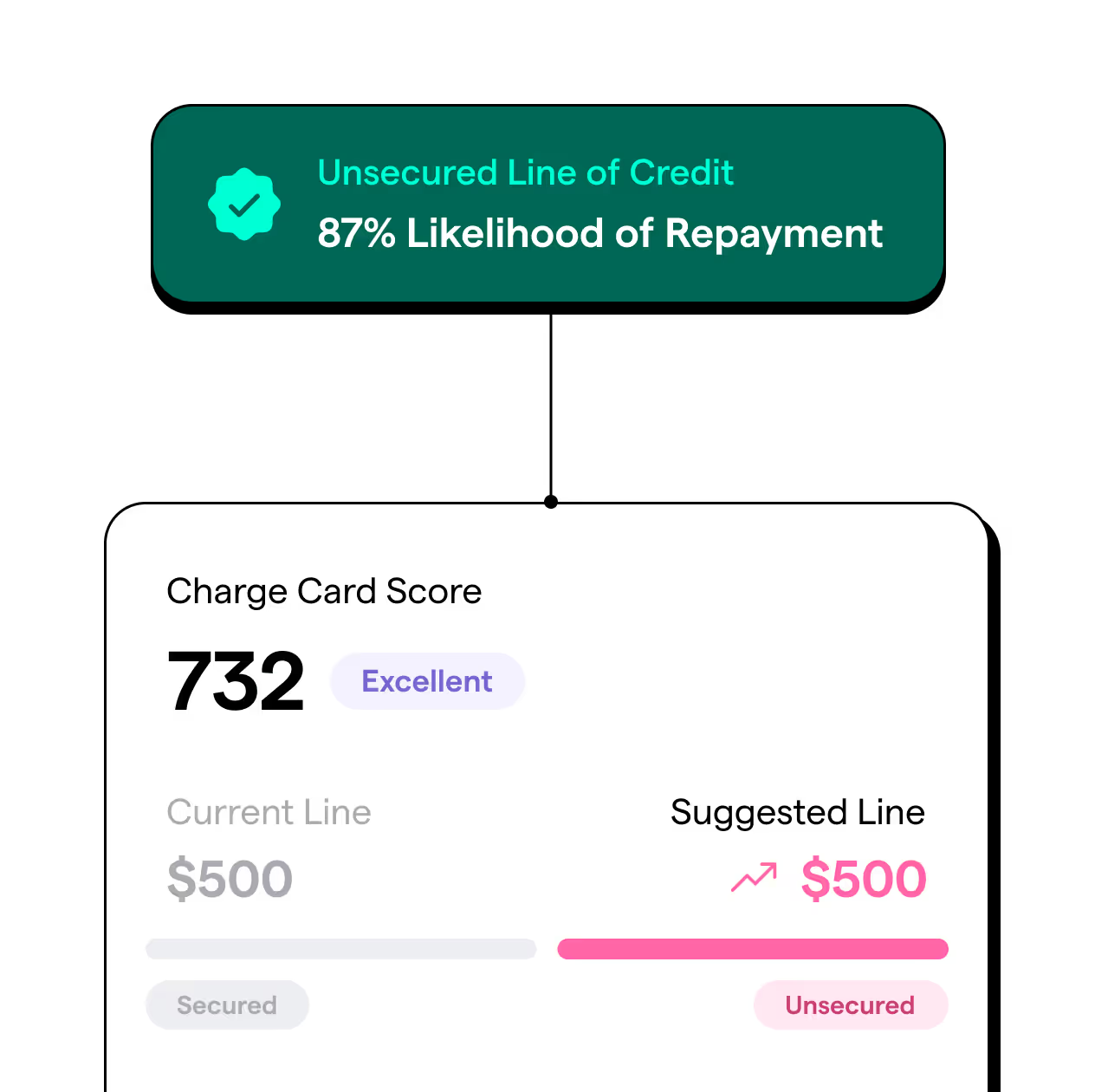

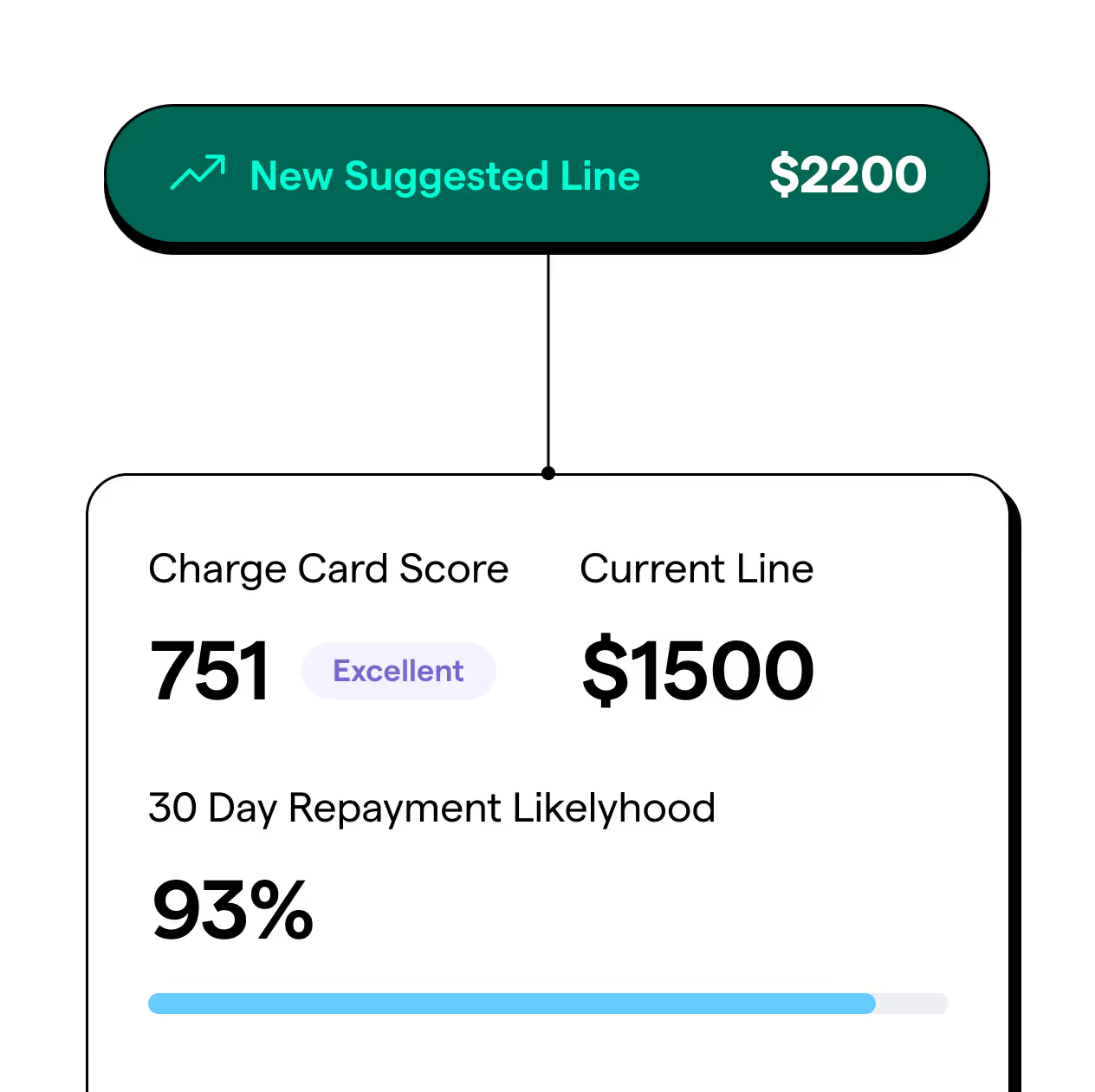

Charge Cards

Graduate users to higher secured or unsecured limits based on increased affordability.

Credit Cards

Set dynamic credit limits based on users' income and affordability.

Drive growth with Cashflow-driven Analytics

Use our Cashflow-driven Attributes and Scores to provide timely, borrower-specific insights tailored to your lending criteria. Make informed decisions that enhance approval rates and loan performance.