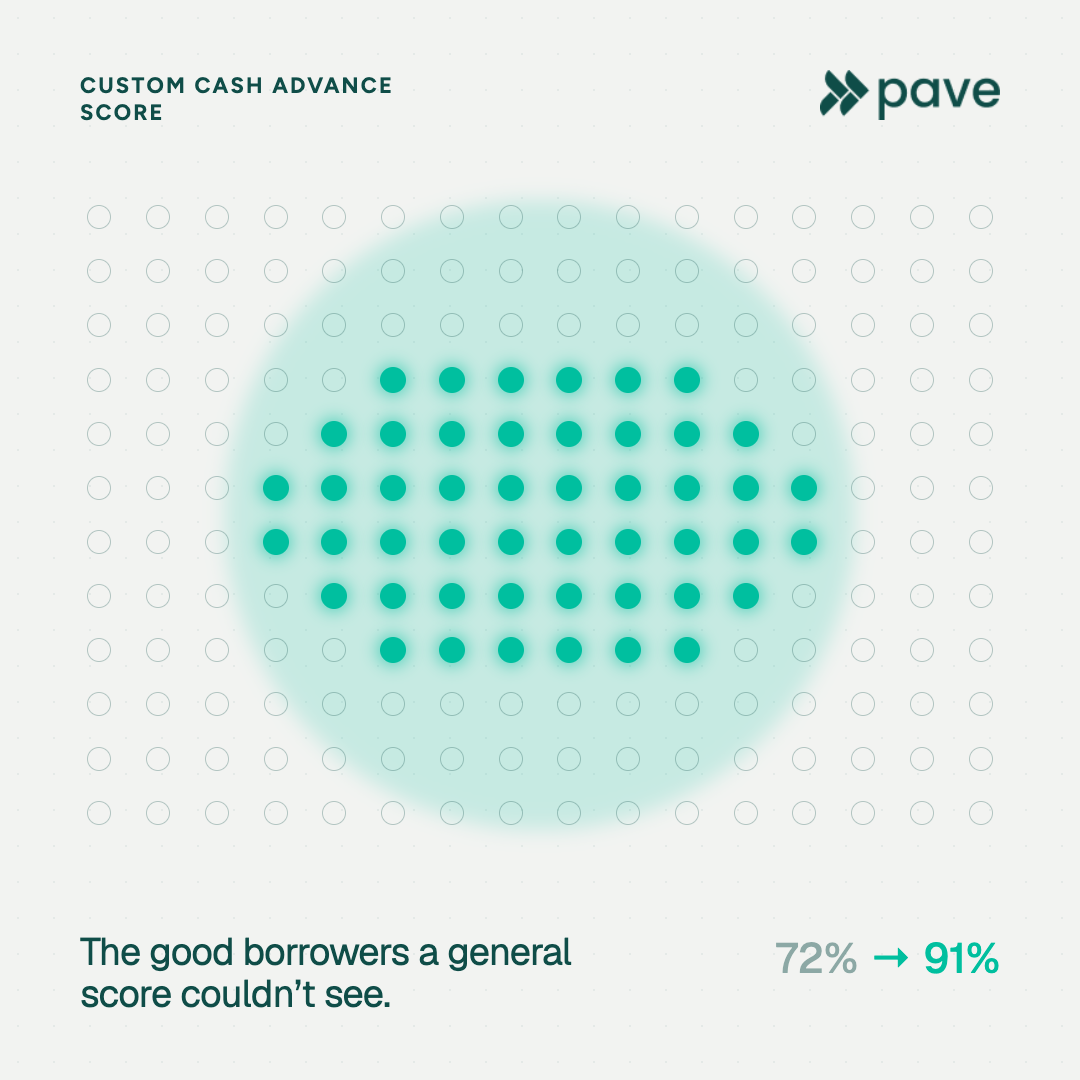

A score built for their book took new-user approvals from the low 70s to 91%

A general-purpose score was turning away good borrowers it couldn't tell apart from risky ones. A score built on the lender's own book found them, and repayment rate barely moved.

Challenge

For a cash advance provider, the new-user approval rate isn't a vanity metric. It's the top of the funnel everything else depends on. Every applicant the model turns away is a marketing dollar already spent, a person who might cancel the subscription or ask for a refund, and a fixed platform cost now spread across fewer funded advances. When first-time approvals sit in the low 70s, that drag compounds across acquisition, retention, and unit economics all at once.

The team was decisioning new-user advances on a general-purpose Cash Advance Score. It worked, but it was built to generalize across many lenders, not to read this provider's specific borrowers. They suspected a real share of the people being declined were good borrowers the general model simply couldn't tell apart from risky ones. The hard part was proving it without loosening the bar and eating a wave of defaults.

So the real question wasn't "can we approve more?" Anyone can approve more. It was "can we approve more of the right people, and prove it before the book is on the line?"

Solution

Pave built a Cash Advance Score on the provider's own advance and repayment data. The design choice was the whole point: a model fit to one lender's borrowers separates good from bad inside that population far more sharply than a model averaged across everyone's. The provider's team owned the score and ran it inside their existing decision flow.

Approach

Results

- New-user approvals rose from the low 70s to roughly 91%, measured against the provider's prior score on the same applicants. A lift of about 20 points.

- 30-day repayment held within about a third of a percentage point (0.003) of the prior model, so the added approvals didn't come at the cost of measurably higher defaults.

The new approvals landed exactly where it hurt before: at the top of the funnel. More approved new users meant less wasted acquisition spend, fewer cancellations and refunds, and platform costs spread across more funded advances, all without accepting a worse book. The custom score didn't lower the bar. It read the provider's own borrowers more accurately and approved good ones the general model couldn't see.

Conclusion

The lesson isn't that custom beats off-the-shelf in the abstract. It's that a score built on a lender's own borrowers recovers approvals a general model leaves on the table, because it tells that lender's good customers apart from its risky ones more precisely. For a cash advance business where the new-user funnel drives acquisition cost, retention, and platform economics at the same time, a 20-point lift in first-time approvals that holds repayment flat changes the math across the whole operation.

The custom score is running in production, and the provider keeps watching repayment as approved volume grows. The signal is strong; the open question now is whether it holds as the book scales, which is exactly what the shared monitoring is there to catch.

See what a score built for your book can do

Off-the-shelf scores you can deploy today, sharpened by every lender on the network.

Explore Use Cases

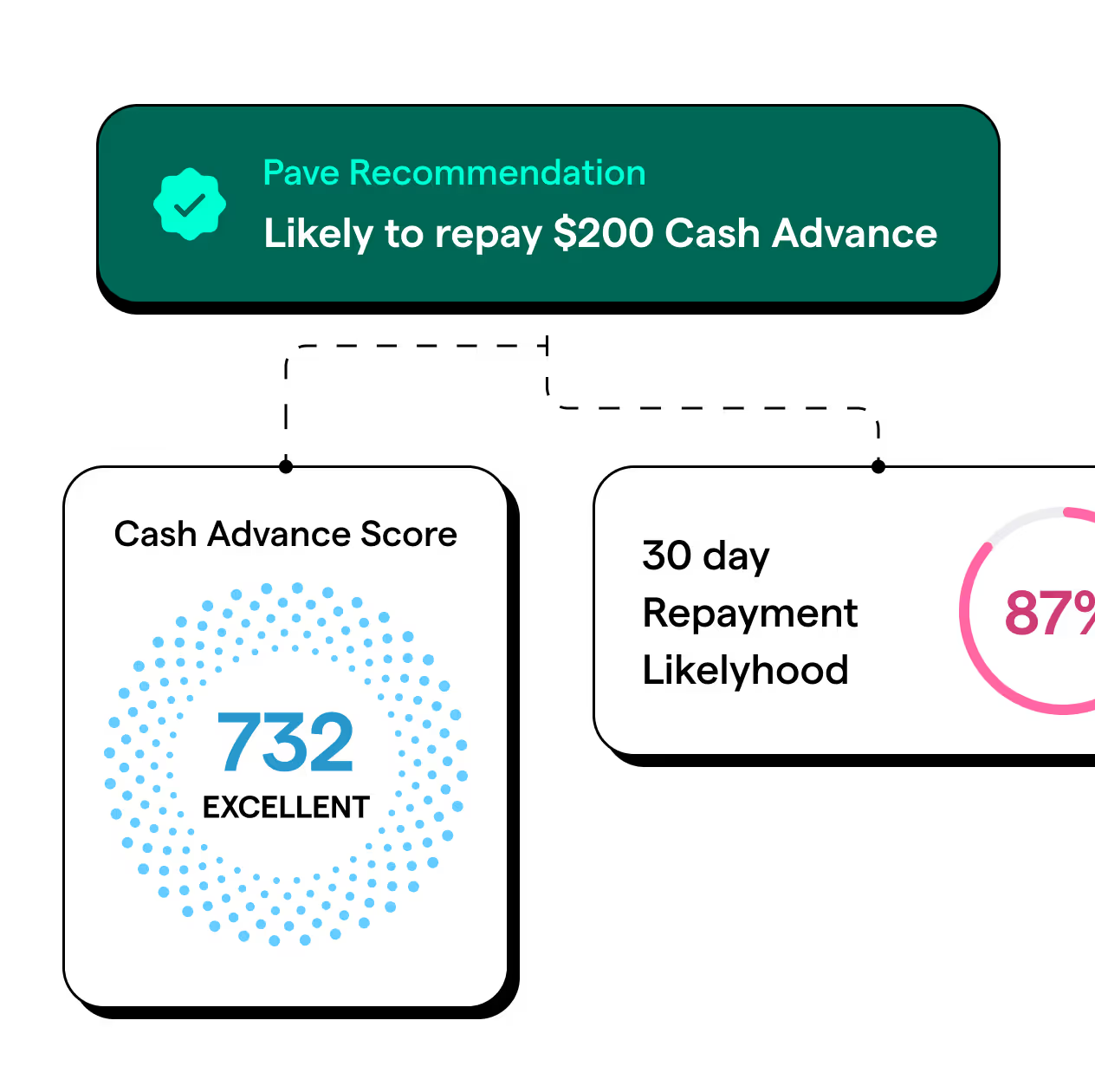

Cash Advance

Score users to increase approvals, advance amounts, and improve repayments.

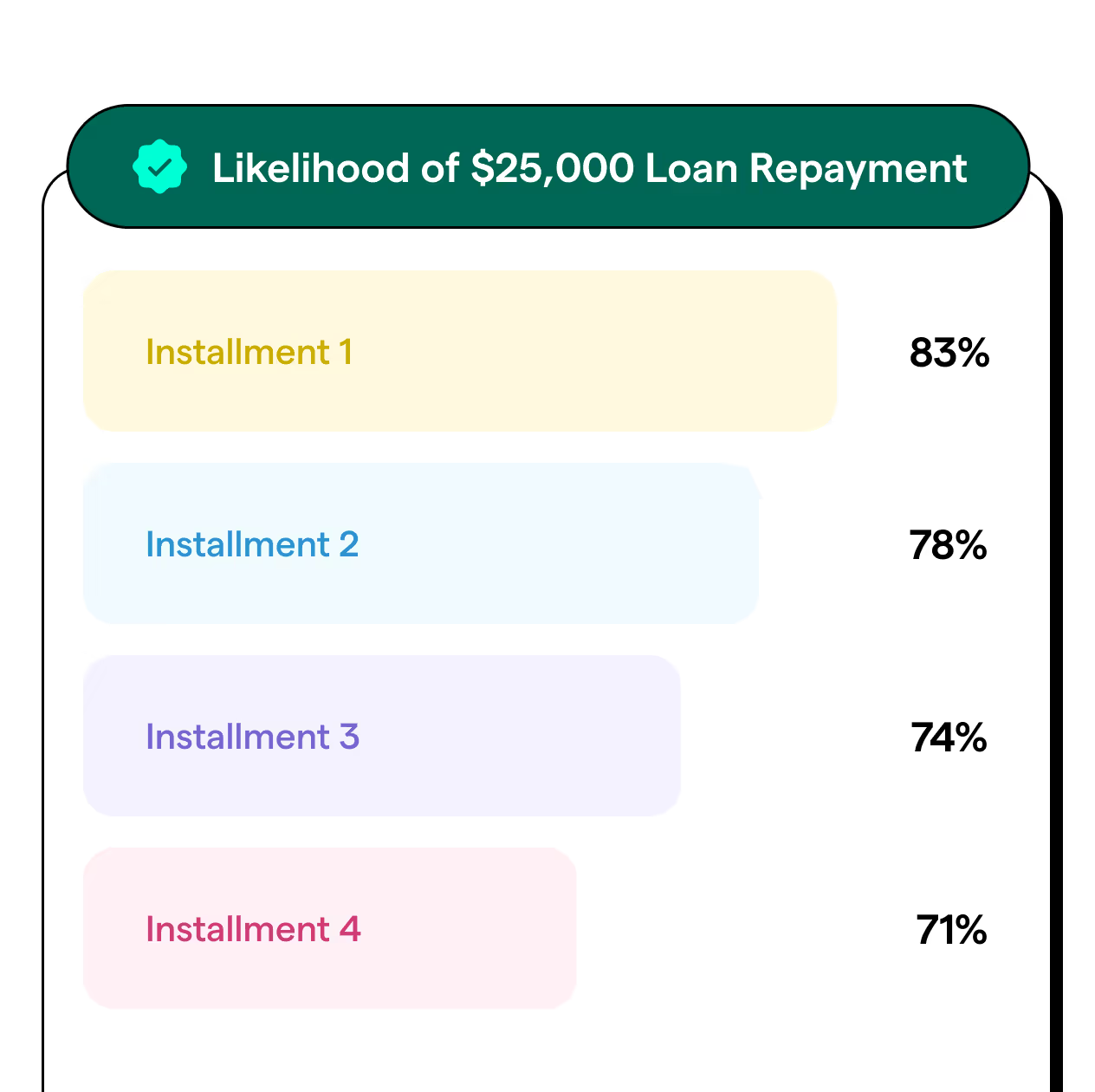

Personal Loans

Identify users with high likelihood of making the first 4 payments to reduce delinquencies.

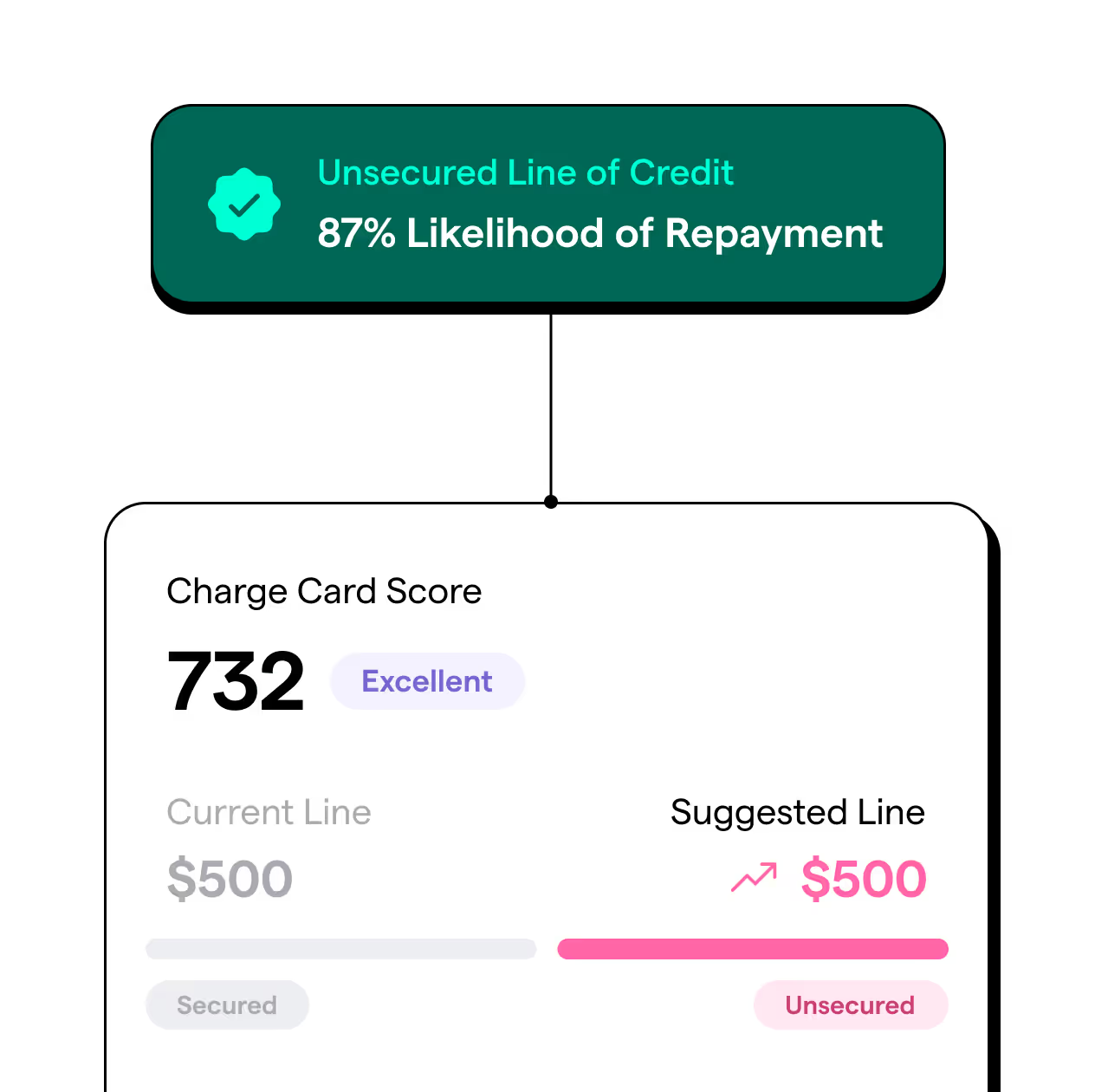

Charge Cards

Graduate users to higher secured or unsecured limits based on increased affordability.

Credit Cards

Set dynamic credit limits based on users' income and affordability.

Drive growth with Cashflow-driven Analytics

Use our Cashflow-driven Attributes and Scores to provide timely, borrower-specific insights tailored to your lending criteria. Make informed decisions that enhance approval rates and loan performance.